When discussing commodity investing, the attention usually goes to oil & gas, iron, copper, lithium, etc.

But the periodic table is much larger than that, and one metal in particular recently caught my attention.

It is required for most military applications from tank armor to artillery shells, air defense, hypersonic missiles, and bullets.

It is also essential in the production of batteries, EVs, and semiconductor manufacturing, as well as mining equipment, manufacturing, etc.

It is at the same time more than 90% sourced from China & Russia, hardly the most friendly suppliers of strategic resources, as a potential global conflict on all the fringes of Eurasia looms large over long-term investing strategies.

I am talking of a metal almost as hard as diamond, and which is out of the radar of most investors, and even most mining companies.

This metal is called tungsten.

Tungsten Primer

Before we get started, let’s get some soundtrack for once. Some quality heavy metal seems fitting:

Tungsten Metal

Tungsten is a pure element of the same family as Chromium and Molybdenum, and maybe unsurprisingly can be used in the same way as these to harden steel.

Tungsten has the highest melting point of ALL known elements, at 3,422 °C (6,192 °F).

Its density is equally exceptional, similar to some of the heaviest elements like uranium (which is also used for its armor penetration capacity in the form of depleted uranium anti-tank rounds). Its name literally means “heavy stone” in Swedish.

In addition, it is mostly non-reactive chemically, making it very hard to corrode or oxidize. Tungsten is found in a mineral called wolframite, from which it got its atomic symbol “W” and its alternative name of Wolfram.

Tungsten Applications

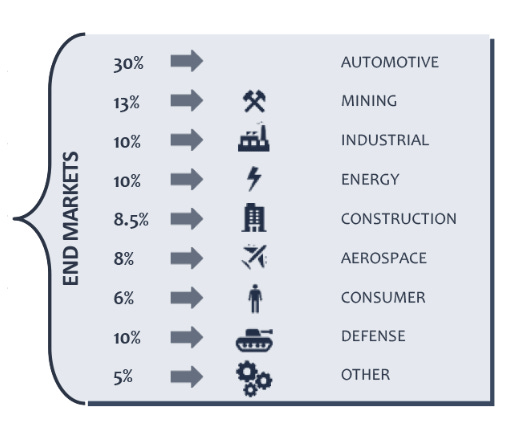

Here, I will list its applications in growing order of importance. I believe that the most solid case for tungsten is military applications, more on that below.

EVs/Batteries

Classical lithium ion batteries are reliant on cobalt, an expensive metal that also tends to be produced from slave labor in Congo. More efficient chemistry has since emerged to try to replace cobalt. One such method is using tungsten thanks to its extremely stable chemical profile.

Other battery technology is looking at tungsten to improve lithium batteries, notably nobium tungsten oxides, which should allow for much quicker to charge batteries.

The startup Nyobolt looking to commercialize this design in partnership with H.C. Starck Tungsten Poweders from Masan High-Tech Materials.

NanoBolt is another battery startup looking at tungsten-based chemistry.

Not central to the thesis, especially with EVs sales slowing down, but still worth mentioning. Especially as it represents 30% of the current demand (see below for an overview of application by sectors).

Semiconductors

Despite its mostly metallic nature, tungsten can be turned into a gas (the densest known gas for that matter, 11x heavier than air) in the form of tungsten hexafluoride.

This allows for depositing tungsten in a very thin 10-15 nanometer layer through the chemical vapor deposition process. This is used in semiconductor production, making use of tungsten’s high stability.

I have not heard of technology increasing tungsten demand for semiconductor, but neither of plans to retire the usage of the metal in the industry.

So overall, the more chips and AI datacenters are built, the more tungsten will be needed for this application.

Mining/Machining

Tungsten’s extreme toughness makes it a perfect metal for metal drills, circular saws, CNC machines, rock stock crushers at mining sites, etc.

Especially in the form of tungsten carbide, which is even tougher and with a higher metling temperature than pure tungsten (twice the density of steel).

This is a rather stable section of the demand, but which might see a boost if mining activities pick up globally in a commodity boom.

Military

Currently around 10% of global demand, tungsten is nevertheless crucial for military applications. It is for example present in both the armor of the M1 Abrams tank and in the anti-tank ammunition.

It is also present in the ammunition of the anti-air/anti-drone system Phalanx I have covered recently. We can assume that a LOT of tungsten is being sent flying at high speed off the coast of Yemen right now.

Others

Tungsten’s properties make it a useful metal in a wide range of other applications. Aerospace is one, especially for rocket nozzles, which is true for missiles as well.

It is also used in construction, surgery tools, X-ray machines, jewelry, lamp filament, etc.

New applications might become important, for example high-temperature (using liquid nitrogen instead ultra-cold liquid helium) superconductors using tungsten are being tested by the Long Island Power Authority.

Overview

The Case For Tungsten

There are three different reasons I decided to give attention to tungsten.

1. The Military Use Case

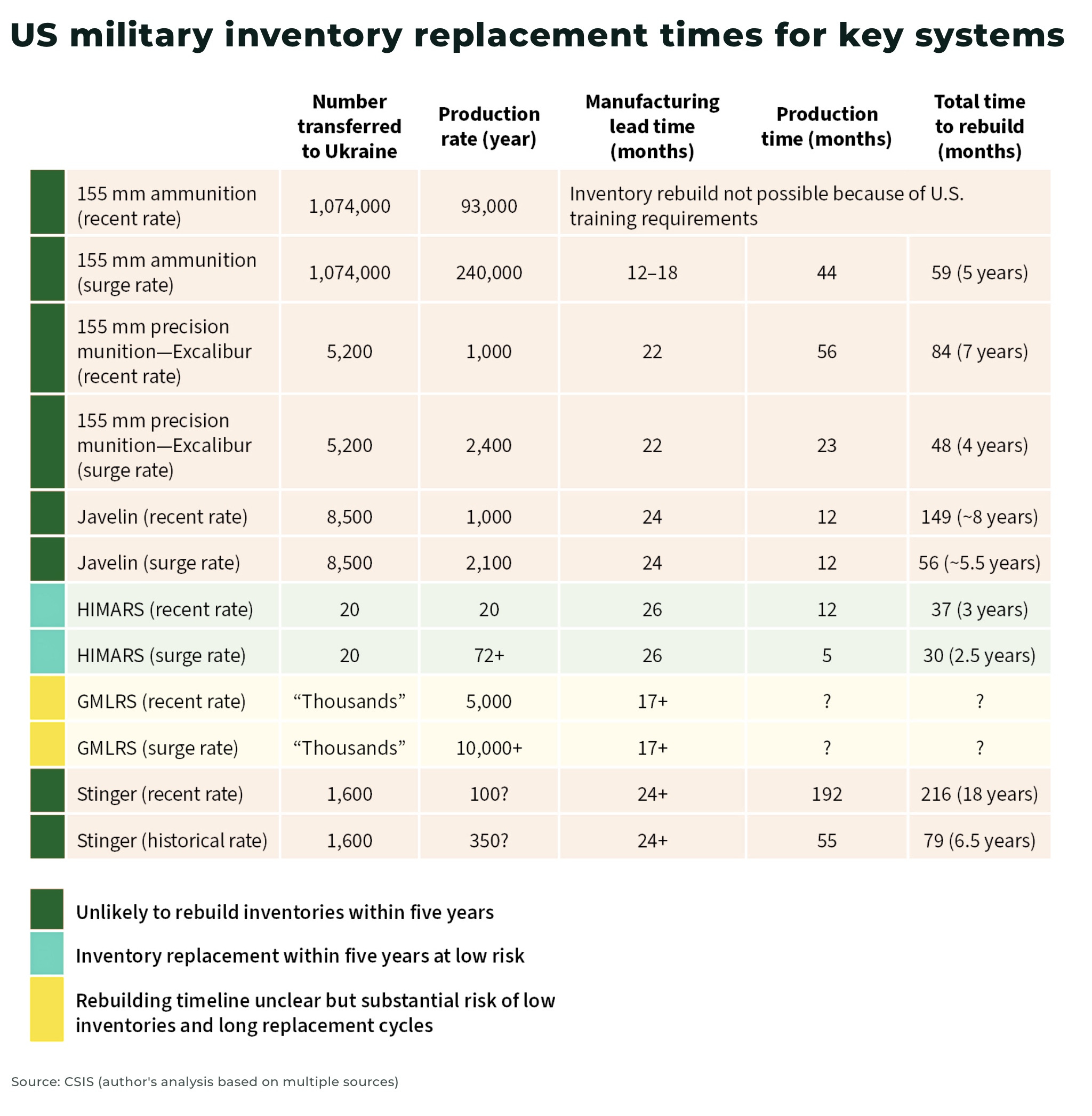

Long-time readers knows the importance I give to how abysmal the West’s ammunition production has been. And the importance of generalized and widespread anti-drone guns to modern warfare.

As a reminder, production needs to be ramped up quickly, as most weapons stockpile need 5-7 years to be replenished.

So it makes sense that we should see a rise in tungsten consumption from this use case alone. Because more tungsten armor is destroyed, more tungsten bullets and 155mm artillery shells are fired, more missile rocket nozzles are burning fuel, and more ammunition as a whole is produced and stockpiled.

And the more advanced the military tech, the more tungsten it requires, for example hypersonic missiles need a lot of it to survive the colossal temperatures created by air friction at Mach 10+.

The other metals coming into weapon production, like steel, iron, brass (copper+zinc) are too common, and with massive civilian uses, for ammunition to move the needle by much.

For tungsten it does.

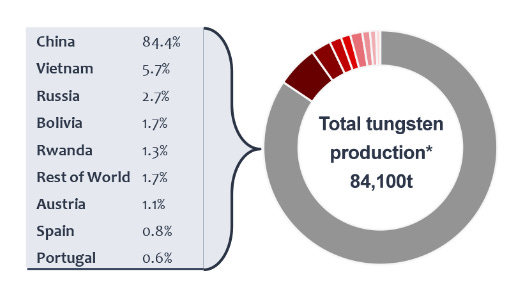

As a cherry on the cake regarding the military question, the immense majority of tungsten supply comes from China + Russia (87.1%) and Vietnam (5.7%), a Chinese ally.

This leaves a remarkably small part of the global production that is geopolitically secured.

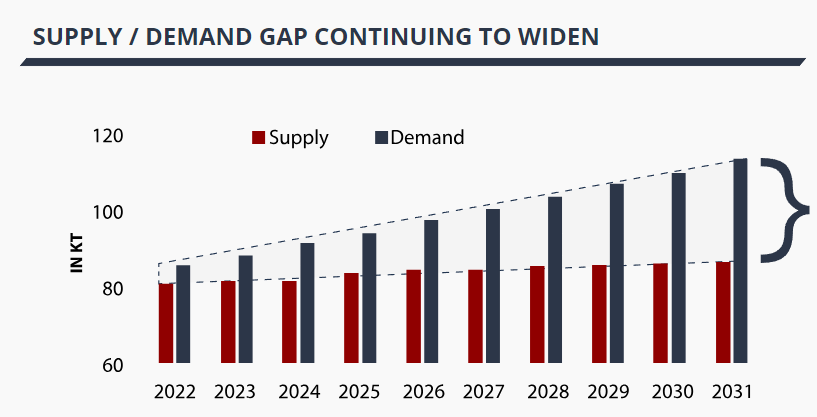

2. Rising Demand - Depleted Inventory

Demand-Production Mismatch

As mentioned before, the demand is growing from multiple angles: commodities production and mining, an aerospace renaissance, EVs, robotics, semiconductors in military demand.

Overall, we can assume a stable or growing demand for the foreseeable future. An average 4-6% CAGR seems reasonable.

The current production is likely already in deficit, although with such an opaque market it is hard to be fully sure. Any increase in demand will be hard to be met by the sector.

And of course, there is the elephant in the room, the threat of export restrictions or a full export ban by Russia and China in the increasingly likely case of escalating conflicts with the West.

And it’s not like they will not need all the tungsten they have to build up THEIR military inventory.

I found one graph showing a gap between supply and demand, but did not calculate the number myself.

In the long term, we should expect supply to somewhat grow, but not in the short and medium-term.

Inventory

It is hard to evaluate the strategic stockpile, but a general trend for the last decade has been regular sales of tungsten by the US Defense Logistic Agency.

In 2022, the US has finally realized they should reverse course and rebuild strategic reserves of “minerals essential to defense supply chains, such as titanium, tungsten and cobalt“.

“the stockpile has been reduced dramatically in size over the past several years [as] the stockpile’s been sold off.”

The stockpile was valued at nearly $42 billion in today’s dollars at its peak during the beginning of the Cold War in 1952. That value has plummeted to $888 million as of last year following decades of congressionally authorized sell-offs to private sector customers. Lawmakers anticipate the stockpile will become insolvent by FY25.

These sell-offs have included 3,000 short tons of titanium, used in building military airframes, and 76 million pounds of tungsten ores and concentrates, used in military turbine engines and armor-piercing ammunition.

“Congress and Pentagon seek to shore up strategic mineral stockpile dominated by China”

Rebuilding that stockpile to its historical level would consume half of the annual global production of tungsten. And that without increasing consumption compared to peaceful times. So we can expect the rebuilding of stockpiles and increased military demand to add another 5-10% to consumption for a few years.

3. A Bombed-Out Sector

Tungsten miners have been out of luck for a long time.

I suspect the reason why China and Russia still have a tungsten industry is that they kept buying it at subsidized prices to keep the miners and smelters alive.

Which by the way probably explains why Russia has no shortage of ammunitions, they actually kept the assembly line running for years, and kept the supply chain alive.

A good example of the average tungsten mine fate in the 2015-2020 period was Wolf Minerals. It had big plans, started production 2015 and filed for bankrucpy in 2018. (The web address of the company is still alive apparently and is now a clickbait link farm…)

You find other miners like this, for example Adex Mining, with a website maybe updated last in 2018 (?). Other miners that had tungsten mines in the past do not mention these assets anymore.

Most other tungsten “miners” are junior exploration companies years from production, with all the money-losing chances that are implied.

As a commodity sector, tungsten is somewhere between a crumbling cityscape and a cemetery.

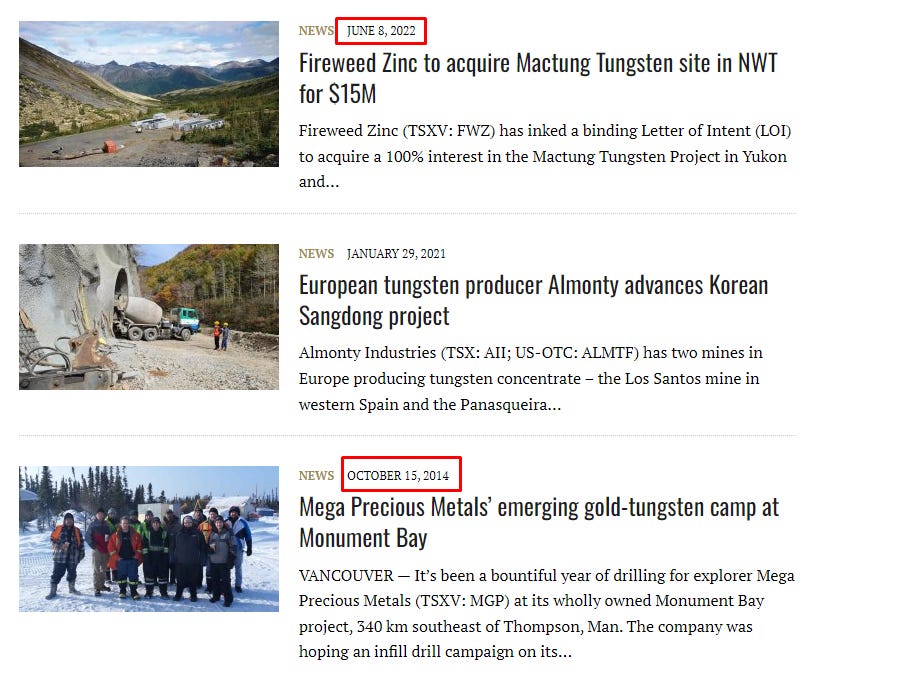

Another indicator of a commodity being out-of-favor is it being completely ignored by the mining press. For example, the search for ”Tungsten” in the mining industry mangazin Northern Miner gives you this:

Not ONE article between 2014 and 2021. Tellingly, 2023 had 4 articles already.

Not unlike rare earth minerals, it took more than a decade for the West to realize their strategic weakness and vulnerability of relying on China + Russia for all their rare metal/uranium/keystone parts supply chain.

Conclusion

Tungsten is a chemically remarkable metal, and a completely unknown segment of the commodity market, even by active traders and investors in the sector.

A big part was due to tungsten’s relative over production in 2015 onward, pushing most miners to bankrupcy. The steady flow of tungsten from strategic stockpiles contributed to the oversupply situation as well.

These conditions are now reversing.

Production out of Russia+China has all but collapsed.

Demand has been rising for years due to semiconductors and EVs.

Military demand is making a surprise come back that will last a decade.

Strategic stockpiles are suddenly switching from indifferent sellers to motivated buyers.

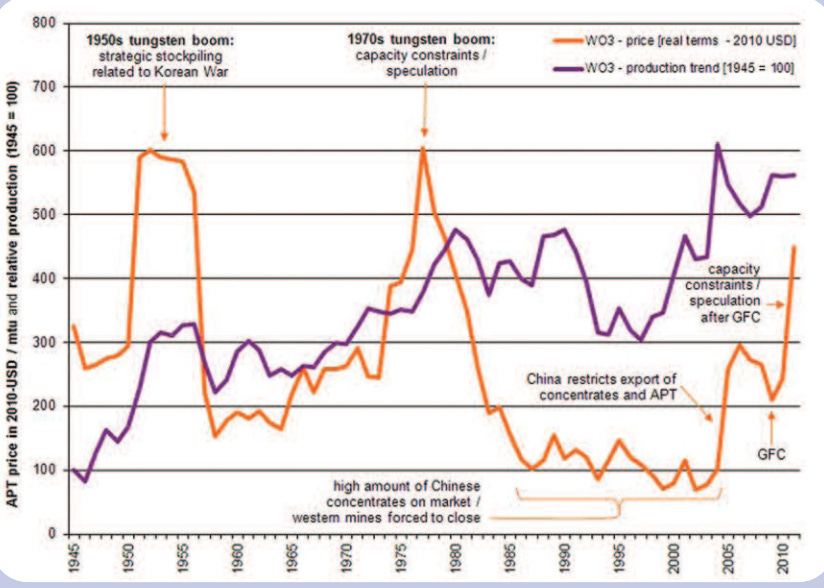

Historically, tungsten prices have boomed either from large scale industrial war (WW2, Korea) or supply shortage after many mines closed.

We are now set up for both.

Target Locked

From my research, there is ONE company that is:

Solvent if not immediately profitable.

Producing tungsten for years (not a junior miner)

Planning to quickly expand its production several fold as soon as 2025, and then several fold again by 2027.

with the expansion mostly already financed and built already.

with a highly profitable guaranteed minimum price.

and NO upper price ceiling.

And this will be the subject of Part 2, the last exclusive report for my subscribers this month.

Armored Portfolio (Part 2)

As I said before, there is a serious lack of tungsten producers out of China/Russia/Vietnam. Most of the other sources are either small-scale, inactive, or artisanal/illegal mining in Rwanda, Congo, and Zimbabwe.