This article will look at the US national debt issue and where we are going from here.

Textbook Exponential

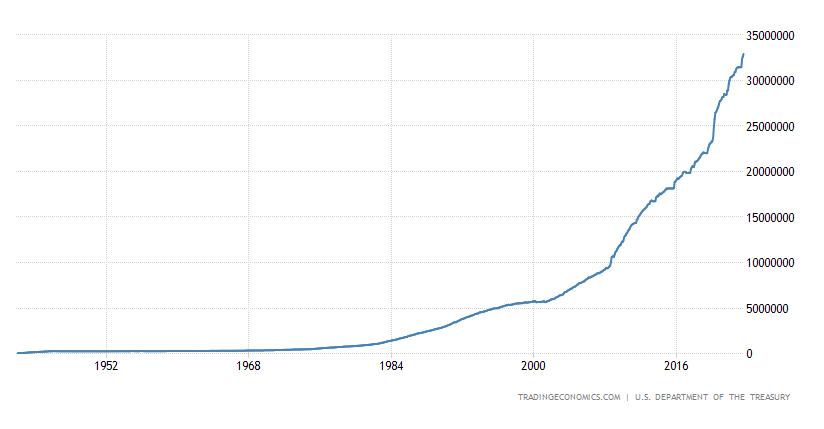

It took the USA from 1776 to 1863 to accumulate the first $1B in debt.

It only hit the mark of 1 trillion in debt in 1981.

So it took 205 years to accumulate the first 1 trillion US dollars of debt.

The next 10 trillion would only take 27 years to be reached, in 2008.

It is now above 33 trillion.

If you know what an exponential looks like, this is as close to textbook as it gets.

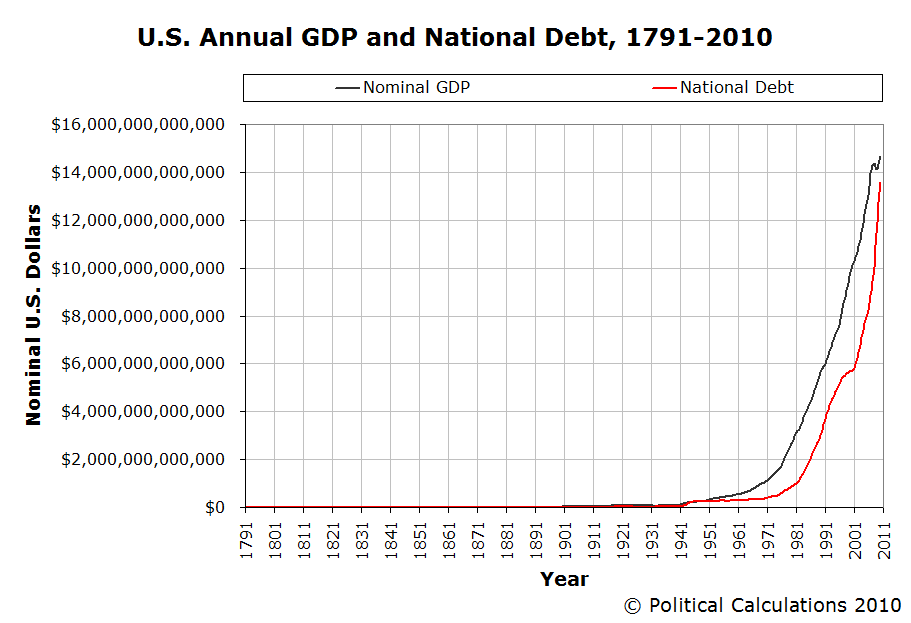

It is even more spectacular if you take the really long view:

You can see how the chart has little dents on the way, each a micro-drama about raising the debt ceiling.

That problem is over, the debt ceiling is now suspended in limbo until 2025. Don’t hold your breath to see it coming back.

Of course, you were told last year to not worry about it:

Speeding Up

In fact, US debt recently grew by one trillion in FIVE WEEKS (or for that matter spikes like $275B IN ONE DAY).

A trillion is such a large number that it starts to make us numb and unable to visualize it. So let’s break it down into something more reachable.

1 trillion per 5 weeks is $5.9B per hour.

$17.9 per hour PER AMERICAN.

$38.2 per hour per ACTIVE American.

Now consider that the average hourly rate salary in the US is $28.34 per hour.

This means that even if every active American had worked 24/7 nonstop (unhealthy I think…) and given the government ALL their income (unpopular for sure), it still could not have covered the new debt taken on by the US government.

And this is not government spending.

Nor is it covering the existing debt.

No, this is only the new debt that would have absorbed the entire country's population income.

Calling it “unsustainable” is a rather hilarious understatement.

Now What?

The Sad State Of Financial News

Among financial media, this is where you would usually get 2 types of commentary:

A ZeroHedge / prepper doomsday article, about how this is the end of the dollar, financial apocalypse any time soon.

A complex and full of jargon article going into M2 money amount, liquidity, Fed swap facility and God knows what other arcane knowledge of macroeconomics that might be relevant or not.

Funnily enough, both are sort of useless.

The doomsday Cassandras are unlikely to provide you with any solid financial advice except to buy gold, and have been wrong on that measure for the last 2 (3? 4?) decades.

The macro guys are mostly busy pushing their reputation as a macro expert, so they can charge you special reports billed in the 5-6 digits, or $500/h consultation. Funnily enough, most macro hedge funds buying those reports lose money; go figure.

I dare to think there should be something else.

Understanding Long Term Trajectory

Debt Crises

Most libertarians and doomsday preppers are not fully wrong. The American Empire is not in its prime and shows serious cracks that are getting more serious by the day.

Where they are wrong is treating it as the end of days.

Historically, too much government debt is a VERY regular occurrence in most nations.

Some are casually doing it every 5-20 years on average, like Greece or Argentina. Some prefer to wait for a few generations between debt crises, in France. And some are more financially sturdy and manage to do so even less often.

So why are these debt crises occurring?

Essentially, because the ruling elite never want to cut their spending. Whether it is to build royal palaces, finance wars or get re-elected, the spending might differ but the situation always shares a common trait:

There are never enough taxes to cover all the mighty ambitions of the enlightened ruler.

It starts with a little bit of borrowing, a little bit of silver in the gold coins.

Soon you add copper to said coins, or force pension funds to buy more government debt.

And when that is not enough, more radical options get initiated like printing money out of thin air. Or attacking other countries to loot them.

What is NEVER considered is the obvious solution: cut spending.

The next war needs to be won, the dignity of the king depends on building this new palace, and the people will never accept a cut on welfare spending.

Until it doesn’t happen.

How Are Debt Crises Handled?

This is THE lesson to remember from history about debt crises.

On a long enough timeframe, EVERY over-indebted government will settle for default or currency debasement over reigning in spending.

Weak countries are forced by their creditor into default and debt restructuring (Argentina).

Strong countries go into hyperinflation (France, Germany, Russia)

Now, the Devil is in the details.

Notice this small “on a long enough timeframe”?

This is the ultimate weakness of libertarian dogmatism.

Yes! One day the dollar will die as a reserve currency or as currency at all.

Like all currencies do eventually.

One day can be a hell of an opportunity cost when your timing is off by several decades.

So if you want to make money during a debt crisis, you need to study what happens BEFORE the ultimate debt default.

Never Buy Bonds In A Debt Crisis

The very nature of a debt crisis is that the government loses control over either inflation, bond prices, or both.

Essentially, this is when too much money printing has flown into the real economy (instead of staying confined to financial assets, real estate, etc…).

From there, inflation either forces the central bank to raise interest rates (sounds familiar) or is left unchecked and gets out of control.

But if interest rises, the government now needs to roll over old debt at a much higher rate, causing the cost of debt servicing (interest) to blow up.

Equally problematic, both corporations and people see their debt burden getting much heavier, squeezed between inflation and rising interest payments.

So tax collection tends to plummet as well, increasing the budget deficit even more.

In case this was not obvious enough, this description matches perfectly the US situation in the last 6-12 months, and this is not an accident.

The problem is therefore that no matter what, bonds will kill you financially.

If inflation stays high, your purchase power will be eroded and the money you get back is not worth much

If interest rates keep rising, the bond’s value keeps plummeting. Currently, US bonds have lost enough in a few years to get back to their 2007 value…

The 60/40 equity/bond portfolio is dead.

But most people don’t know it yet and are pilling up MORE MONEY in bond markets.

The Loooong Debt Cliff

If you keep playing with fire, you will eventually get burned.

The same holds true with excessive debt.

It does not matter until it does.

And when it does, you have left the edge of the cliff for a while.

But the process of running over empty ground and starting to fall can take a long time in real life.

To give an example in history:

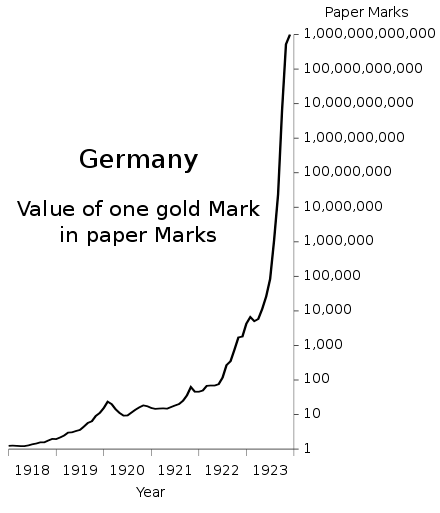

In 1914, WW1 started, and with it, every major European power went into debt to finance the war.

In 1918, Germany loses the war.

In 1921, 7 years later, inflation starts to pick up.

In 1923, the Ruhr Crisis finally pushes the Deutsche Mark over the edge and hyperinflation starts.

In 1924, 1 trillion paper mark notes are converted into 1 new Reichsmark, worth $0.23.

Prices somewhat stabilize in the 1925-1926 period.

Then a new shock of mass unemployment hits the country with the global 1929 Great Depression.

There were also many periods of disinflation, sometimes as dramatic as the mark recuperating 60-80% of its purchasing power in a matter of a few months.

So following the short-term news cycle was VERY dangerous. It was a recipe to see the tree (short-term fluctuations) and miss the forest (the long-term direction). Any parallel to the “inflation is over” narrative these days is not accidental.

Weimar is somewhat unique in that the excess spending was due to war reparations. This made spending exceptionally inflexible and left little option for the German government. One could even say it actively courted hyperinflation as a way to escape reparations payments and give the figure to France and the UK.

So this is a case where the inflation went out of control comparatively quickly.

And still, it took an entire decade to play out.

In comparison, the French Ancient Regime and its economy would limp on from the Mississippi bubble in 1720 up to the French Revolution in 1789. A whole 69 years of monetary distortion and economic mess.

An entire lifetime.

Wile E Coyote can stay in the air a damn long time…

I am not sure how long the US will take, but my bet is not for a quick resolution.

How To Play A Slow Burning Monetary Collapse

Via Negativa

Nassim Taleb is famous for insisting that what matters the most is what you do NOT do.

So the first thing is to know what to avoid. Bond markets are the sacrificial lambs in this situation.

As they are waaay larger than the equity market, this is a source of capital to drain that will last a while.

Banks Are Fine, Kind of

And the government has a strong incentive to keep the process organized.

So we are unlikely to see a banking collapse. Individual banks, yes for sure, we already had an appetizer of it with the collapse of the Silicon Valley Bank, triggered by losses on bonds.

Nothing that cannot be papered over by liquidity fresh money printing from the Fed. It worked in April 2023, it will work in 2024, 2025, etc…

If you believe the Fed will let the entire banking system go belly up, you do not understand history or politics.

Once again, ZeroHedge-style catastrophism is detrimental to your financial health.

The alternatives will be either:

yield curve control (YCC), printing money to keep bond rates low enough, reigniting inflation.

decreasing interest rates, and reigniting inflation.

stop interest rate rise and keep it flat, perform the occasional bank rescue, and let inflation “stabilize anywhere between 4-10% yearly.

Employment Stays High

A surprising characteristic of a high inflation environment is also a high level of employment. There was no mass of unemployed people in the Weimar Republic, that came much later as a consequence of the Great Depression.

So people have jobs, but their salary real purchase power is constantly declining. Forcing them to work more, take a second job, etc… just to keep up.

Any parallel to US worker situations is not accidental.

If the Fed waits for unemployment to rise to stop raising rates, they might wait a loooong time.

This is because of what is called a “crack-up boom”. Rising prices boost immediate consumption, as people buy everything they can before prices go up. Companies do the same.

This flurry of purchases caused an illusion of an economic boom, while also increasing money velocity and inflation further. In modern economic descriptions, this is partially what central bankers called “embed inflation expectations”.

Debt Is Great! Wait, What?

If variable-rate debt is bad, because rising rates can kill you before the finish line, fixed-rate debt is great.

For a micro-economic example, I currently hold a 10-year fixed rate loan at 4.8%, because of subsidies on green loans. Last year, my rooftop solar panels paid their loan, and then some more, while my real interest rate was a MINUS 15%.

If you can find a bank stupid enough to give you money at an acceptable fixed rate, the best day to take a loan was yesterday. The second best is today.

Remember, No Leverage!

While long-duration fixed-rate debt is almost free money, leverage is deadly in a highly volatile environment.

We are talking of potential +/-30% or even 50% moves in a matter of a few months not unlikely by the years 2025-2028. Any 1:2 leverage ratio will turn into a deadly margin call in such an environment.

The Best Equity Profile

The take on debt works for corporate bonds as well.

If a company has very long-duration bonds on its balance sheet, there is a nonzero chance its real cost will be essentially zero by the time we reach the 2030+ date for repayment.

If holding bonds is equal to having a death wish, selling these bonds is a true bonanza.

Short-term debt requiring refinancing in the next 5 years is however highly toxic.

Time to dig deeper into these annual reports! A major debt crisis is not friendly to the lazy analysts.

This holds true only if the company has real purchase power and its sales prices can keep up with inflation.

Harder done than said, but this is the general template: pricing power AND a high level of long-duration debt.

The Making Of Inflation Kings

Generally, productive real assets in an exporting industry are ideal. This was the template followed by Hugo Stinnes, who became the richest man in Germany during the Weimar hyperinflation and earned himself the title of Inflationskönig, or“inflation king“. His playbook was simple:

Take on debt to acquire coal mines, steel mills, etc.

Export their product, getting access to hard currency (good-as-gold dollar, francs, pounds).

Using the hard currency to reimburse debt in now much devaluated Deutschmarks.

Use the now debt-free assets to raise even more debt.

Rinse and repeat.

A key component here is having the right connections in politics and banking to keep getting access to debt funding.

Real productive assets like mines, factories, or even woodlands, are better than let’s say real estate, which might struggle to collect rents and whose value might fall in real terms.

Thinking The Transition Ahead

The reason why so few people make it to the other side of a monetary crisis is that you need to be extremely flexible.

Hugo Stinnes’ empire would fall apart in 1925 when his formula finally stopped working and he did not know when to call it a day, cash in his chips, and leave the casino.

High debt repayment that inflation was no longer covering turned crushing. High taxation level as well.

We are several years away from that point, but it is worth remembering ahead of time.

What worked yesterday (high flyer tech stocks, bonds) will not work today. What will work today will not work tomorrow.

Firms that mushroomed during the inflation, now found that the real interest they paid on loans for the first time was positive rather than negative, though the rates appeared to be lower.

Perhaps most significant was for the first time they were obliged to pay real taxes, many of which were extremely high because of the necessity to rapidly balance the budget and to bring official salaries, which had fallen disastrously, up to an acceptable level again.

Companies were often unable to buy new machinery after stabilization came, so much so that huge stocks of unsold iron and coal began to build up in the Ruhr. Not even the foreign loans flowing in were able to prevent the seizing up once again of the Ruhr mining industry where pit after pit, especially any producing poor-quality coal, was forced to close.

When Money Dies / Wealth Playbook