In Part 1, I discussed how to manage South America’s political risks.

In this article, I wanted to look at the country that has had by far the largest presence in my portfolio in the last 2 years, Brazil.

Investing In South America - Managing Political Risk (Part 1)

Never Boring South America is a true emerging market sector for investors. This is a place where stocks are cheap, and profits SEEM easy. It is also a place where fortunes are lost and made. More often than not, lost… And it is the geography that appears to me the most attractive in the world right now.

The Brazilian Rollercoaster

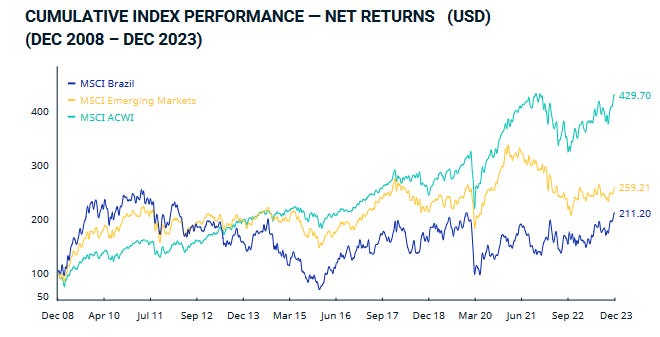

Saying that the Brazilian stock exchange has had a tumultuous decade is an understatement.

In 2008-2010, the country was at the top of a commodity cycle, and fell victim to the Economist’s cover curse:

As you can see in the index performance from MSCI, Brazil in 2020 was at the same level as in 2008, or a whole 12 years of sideway moves, with a lot of volatility.

Even with the recent catch-up, Brazil is still underperforming other Emerging Markets (EMs) and the global world indexes.

This abysmal performance was partially due to coming out of the highs of the 2000s commodity bubble. And partially due to excessive state spending and corruption accumulated during the Lula and Rousseff years.

Brazil conformed well to my method of evaluating political risks in South America:

One moment to enter the Brazilian market was at the end of Dilma Rousseff's presidency, who ended impeached (peak leftism).

And the best moment to sell was after years of improving conditions, culminating with the end of Bolsonaro’s presidency (peak rightism).

Brazil’s General Data

Most of Brazil’s population is located on the coast, with most of agriculture done in the inner highlands. It is the 5th largest country in the world.

It makes up almost half of South America's population, the 7th largest country by population with 203 million people. It has a slightly aging, but stable population.

Its GDP is $2,1T and $10,412/capita. In PPP, it has a GDP of $4.1T and $20.412/capita.

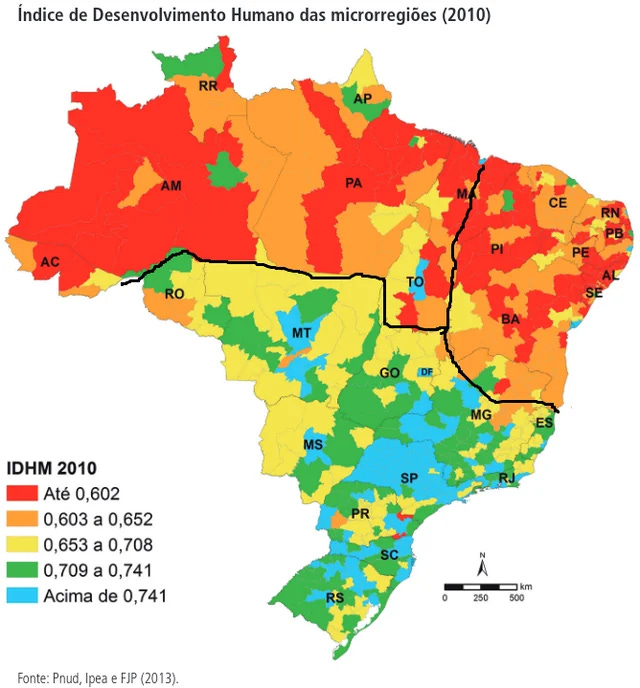

Overall, the more South a region the richer and more developed it is. This correlates with a racial divide, with more descendants of slaves and natives in the northern states.

Brazil’s Economy

As mentioned in Part 1, Brazil is a serious industrial power, with 29% of its GDP coming from industrial activity.

This is in part due to industries transforming raw materials into semi-finished products (refined sugar, aluminum, etc.) and partially a strong domestic and regional base for consumer goods (cars, appliances, etc.).

But when it comes to exports, Brazil is very much a commodity superpower, with a strong presence in agriculture, timber, metals, and energy.

Agro + timber products

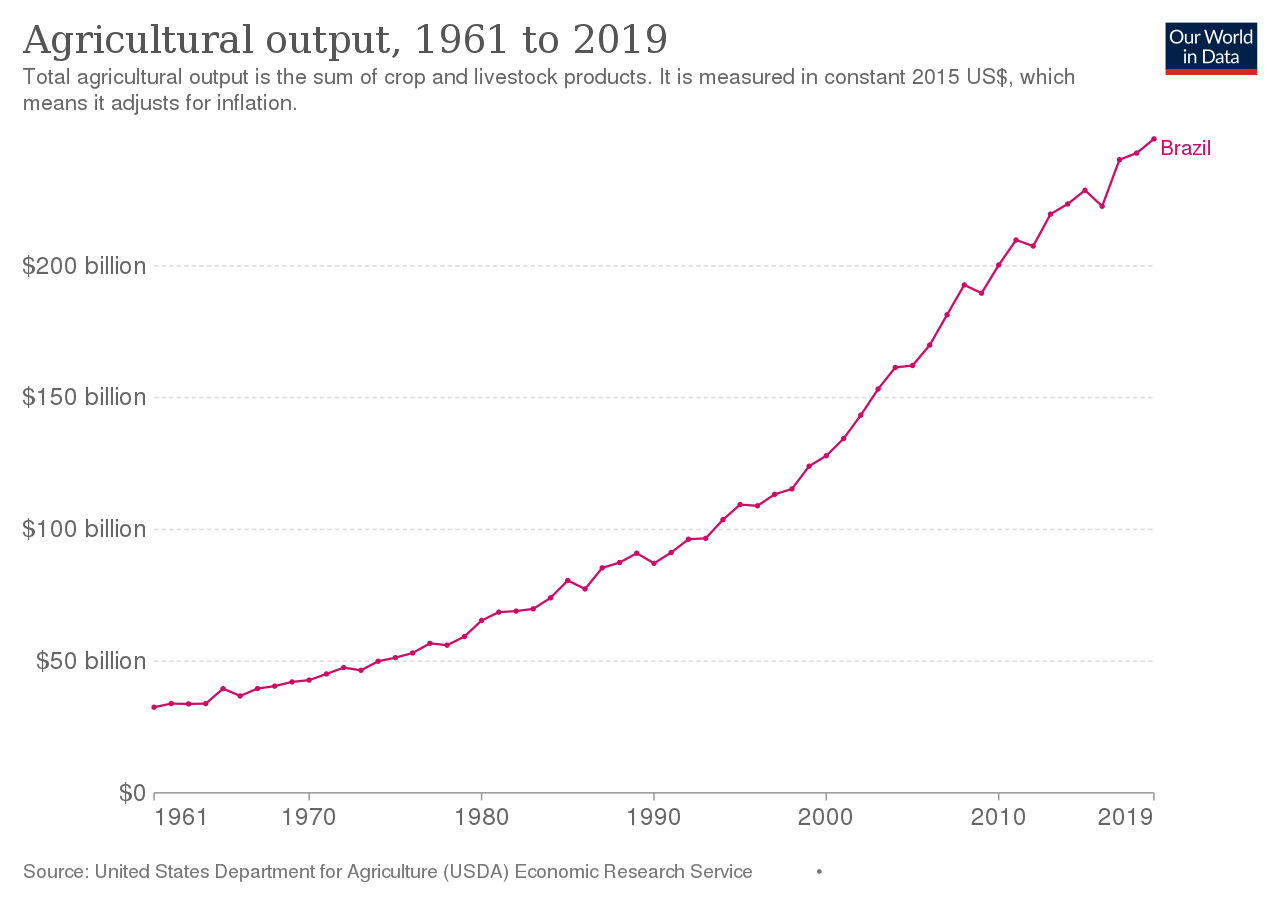

Brazil's food production has multiplied in value 7-8x since the 1960s.

Its production is ranked globally:

#1 in sugar, more than double than that of #2 (India)

#1 in soybean

#1 in oranges

#1 in coffee

#1 in guarana (twice the caffeine content of coffee beans)

#1 exporter of chicken meat

#2 in tobacco

#2 in beef

#3 in maize

#3 in beans

#3 in pineapple

#3 in banana

#4 in cotton

#4 in watermelon

#4 in pork

#5 in cassava/manioc (an important potato-like tuber stable crop in the tropics)

#5 in coconuts

#7 egg producer

Maybe more controversially, Brazil is also an exporter of timber, both native Amazonian forest and cultivated timber. The sector is worth around $6B annually.

A positive development is the growing popularity of agroforestry, where timber is grown with grassland and cattle, providing shade and moisture to the grass and cattle as well as building soils. And an extra & valuable “crop” once the timber is fully grown every 20+ years.

Metals

The mining segment is remarkable:

iron

bauxite (aluminum)

nickel

manganese

niobium (98% of the world’s reserves) in Brazil

gold

gemstones

Brazil is the second-largest iron ore exporter (behind Australia) and among the top 5 of bauxite. Brazil is the world's largest producer of amethyst, topaz, and agate and is a big producer of tourmaline, emerald, aquamarine, garnet, and opal.

While illegal mining in the Amazon happens, especially for gold, the issue is less widespread than you might think. In value, this is a slightly smaller sector than other commodities like food and energy.

Energy

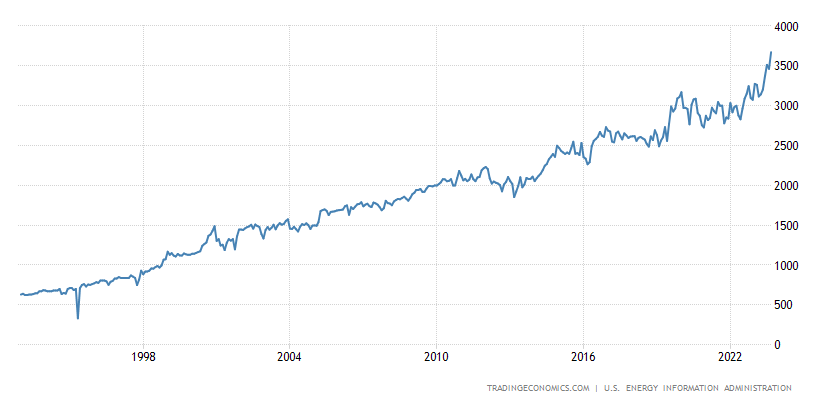

Since the discovery of oil off the coast of Brazil, the country has steadily grown its production.

Rosy forecasts of more production growth predicts Brazil to become an even bigger oil producer but be warned that previously, such a forecast has always fallen short. So we should expect a steady growth of production, but nothing meteoritic either.

As it is heading for 4 million barrels per day, this puts Brazil just above the UAE & Iran, and just below China and Iraq.

So it is fair to say that Brazil is not yet a true oil juggernaut like Saudi Arabia, America, or Russia (9-12 Mbpd), but among the serious players nonetheless.

Brazil currently consumes 2.5 Mbpd, allowing its growing production to be a serious money maker and export for the country.

Most of the oil production is under the control of the national oil company Petrobras, with some other offshore blocks managed by other companies, notably the Chinese CNOOC.

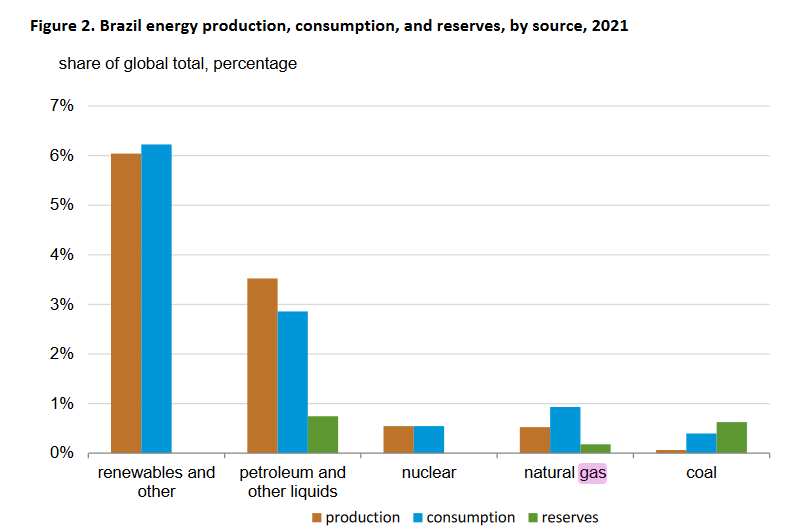

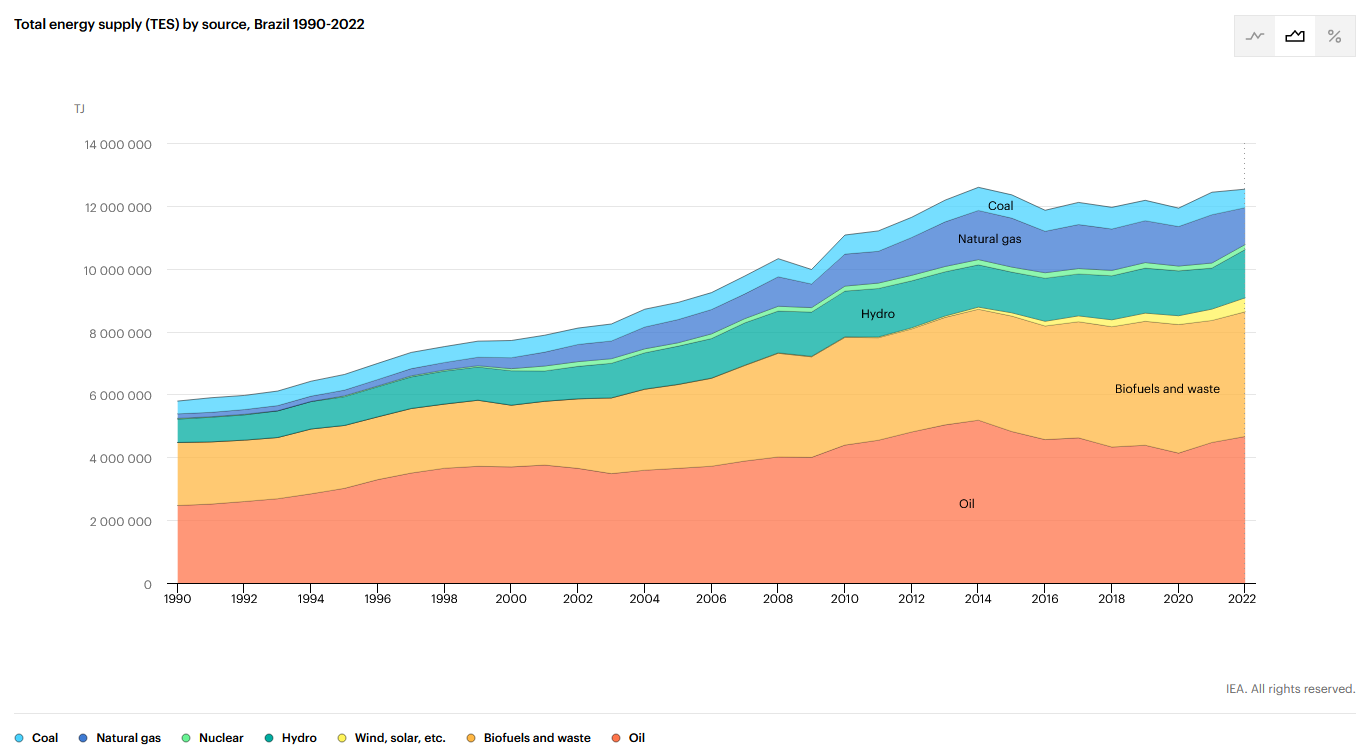

The country also produces some natural gas, but is far from a powerhouse in that sector, even if it covers its demand.

When looking at the total energy supply, biofuels and biowaste from the massive sugarcane production make for a unique volume, almost as large as oil itself.

This raises the question of fertilizer imports, as this level of agricultural (and apparently energy) production is heavily dependent on fertilizers. The fertilizer imports are no less than $16B per year.

Of which $4.4B is nitrogen fertilizer, which is essentially transformed natural gas, and mostly should be considered as energy import.

Brazil is the #1 importer of nitrogen fertilizer, primarily from Russia ($1.08B), China ($641M), Qatar ($638M), Nigeria ($405M), and Algeria ($404M). 95% of potash is imported.

The country is actively looking to reduce this dependency. The growing surplus of gas is a natural candidate to develop local production but might fall short of total demand.

Some projects to grow the local potash and potassium supply exist as well, they are mostly privately held from what I could find.