Investing In South America - Managing Political Risk (Part 1)

The Counter Intuitive Path To Profits In South America

Never Boring

South America is a true emerging market sector for investors. This is a place where stocks are cheap, and profits SEEM easy.

It is also a place where fortunes are lost and made. More often than not, lost…

And it is the geography that appears to me the most attractive in the world right now.

Quite a few news have put the region back in the spotlight recently:

The messy power transition during the election of the new Brazilian president.

The election of turbo-libertarian Milei in the eternal basketcase Argentina.

The rise of strong man Nayib Bukele as Salvador's president and his successful crackdown on gangs.

The threat of a Guyana Invasion by Venezuela.

Massive strike in Panama leading to the closure of First Quantum’s copper mega-mine.

And that’s just for the largest, most discussed events. Columbia, Peru, and other countries in the region provide plenty of political turmoil as well.

So how can investors navigate these troubled waters, and are the cheap valuations just siren’s songs waiting to kill the naive sailor?

A Quick Overview

Before going further, let’s just give a quick look at the region.

General stats

The place is home to 434 million people and has a GDP of $3.6T ($7.6T in PPP).

For comparison, the EU has 448 million people with a GDP of $17.8T ($25.3T in PPP).

This puts South America firmly into the emerging markets category, although a relatively rich segment of it, with $8,340/capita GDP, lower than China’s $12,556/capita and almost 4x larger than India’s $2,256/capita.

I need to emphasize this. The times to see South America as a place of favelas and narco warlords are mostly over. Not all of these issues are fully resolved, but investors will need to see it as a place with a growing middle class, rising level of literacy and education, and overall becoming safer.

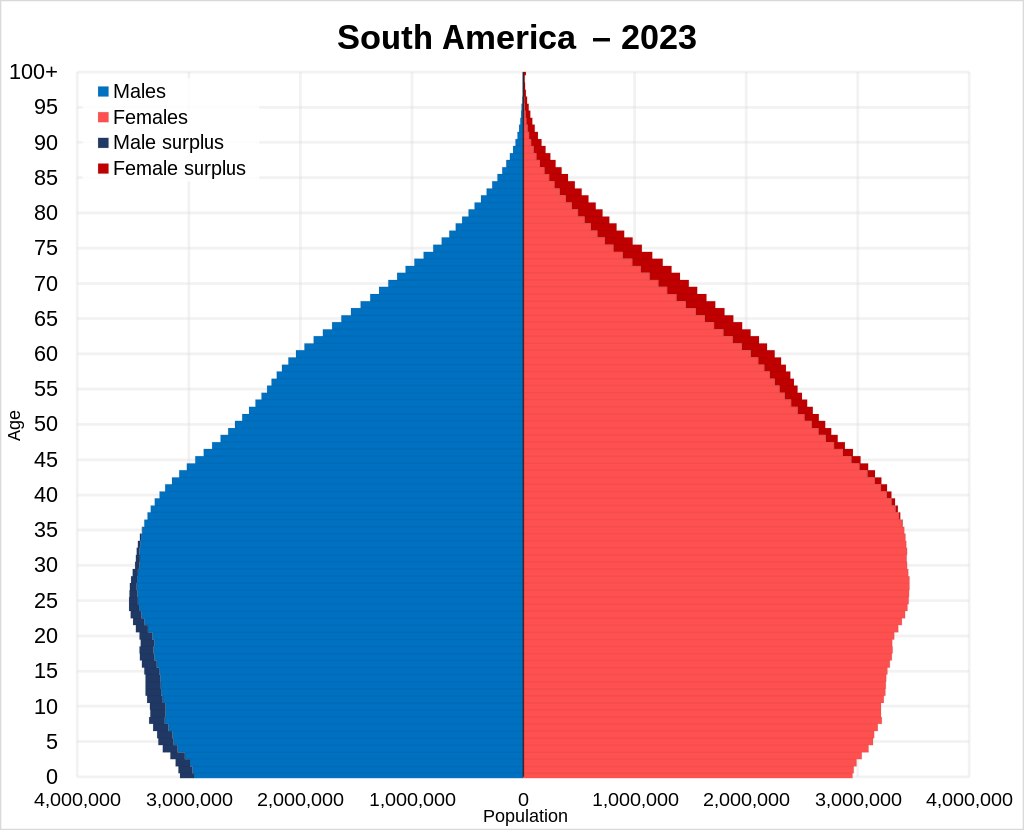

The population is not that young but also has a rather balanced age pyramid. This is an area that has achieved demographic transition (avoiding the overpopulation issues of India and Africa), but far from a demographic collapse (avoiding the quickly aging issues of the developed world and East Asia).

By far the juggernaut of the continent is Brazil, with almost half of the population (217 million people) of the whole continent. The next large countries are:

Colombia: 47.6 million people.

Argentina: 44.2 million.

Peru: 31 million.

Venezuela: 31.3 million.

Chile: 17.7 million.

Literally, every top 20 large population center of the continent is located in these 6 countries.

The region is speaking either Portuguese (Brazil) or Spanish, allowing for homogenous business operations for multinationals and easy cultural exchanges. The common inheritance of Spanish colonialism also creates a relative cultural homogeneity.

However, the geographic barriers of the Amazon jungle and the Andes have created a pattern of regional isolation, and a population density mostly hugging the coastline.

Economics

Raw materials

The export of energy (mostly oil), foodstuff, timber, and metals are the core exports of the region.

When it comes to farming, Chile, Argentina, Brazil, and Colombia are in the top 5 exporters of almost everything: coffee, cocoa, tobacco, sugar, maize, soy, rice, fruits, pork, beef, chicken, natural rubber, palm oil, etc.

The mining segment is equally impressive, with massive deposits of:

iron + bauxite (aluminum) + nickel + manganese + niobium (98% of the world’s reserves) in Brazil

copper + gold + silver + zinc + molybdenum + lead + tin + antimony + in the Andes

lithium in Chile+Argentina+Bolivia

It is no exaggeration to say that resources from South America are feeding and building the world.

Industry

Contrary to the image of just a raw material provider, South America is also a strong industrial region. 29% of Brazil’s GDP comes from industrial production. The region is mostly self-sufficient in most goods like cars, appliances, textiles, as well as chemicals, steel, cement, etc.

The reason why this is not well known is that these industries are poorly connected to the world’s supply chain. They produce for the region but export little.

High-tech industries like semiconductors, biotech, etc. are notably lagging or even almost absent. Managing to develop local expertise and global champions will be key to the region's chances to escape the Middle Income Trap, a term created to describe South America's relative economic stagnation.

Services

The services sector is definitely underdeveloped, due to historically poor infrastructure. The spreading of high-speed internet is changing that, with several impressive fintech companies emerging from the region like MercadoLibre.

Geopolitics

Overall, a great asset of South America is its distance from the Great Powers’ struggles. While the continent has been roughly under the tutelage of the US (Monroe Doctrine) for the last 2 centuries, it is not a battlegroup for influence.

This might change in the long term, but realistically not for at least another decade. Russia is barely present here. China is the main trading partner but seems uninterested in interfering as long as raw resources keep flowing.

And would it want to interfere, it could not do much besides economic carrots and sticks, lacking entirely of expeditionary capabilities or a blue water fleet.

With the borders of Eurasia burning or at risk of exploding in Ukraine, Israel, Yemen, or Taiwan, this alone should put South America on investors’ radars.

Politics

The resource wealth, dynamic demography, and solid industrial base should make South America very attractive to global investors.

The issue is politics, with the countries in the region famous for shooting themselves in the foot on any given occasion.

South America is notorious for its regular surge of left-wing populism, nationalization, and Marxist insurgencies, interrupted by right-wing dictatures and repression.

It can be blamed partially on the inheritance of colonial institutions, poor rule of law, or slavery. The result is a perenially unstable political situation, with the pendulum constantly oscillating widely between far-left and far-right.

This caused the eternal objection to any investment idea located in South America.

“It is cheap but the expropriation risk is too high if THIS GUY becomes president”

The alternative versions include “The politicians will just steal all the money”, “corruption is too high”, and so on.

Which is a fair point. Countries with a history of corruption tend to stay corrupt.

How To Manage Political Risk

Which brings me to the point of this article.

A VERY common idea is that investing in a South American country is too dangerous if the president is left-wing.

I actually think this is the opposite, and that an established left-wing government is the ideal moment to invest in South America.

Let me explain.

Fluctuating Perceptions

The perfect example is given to me by Argentina, by far the most dysfunctional political system in the continent after Venezuela, and that’s saying something.

Argentina has gone from being richer on a per capita basis than Western Europe to a country plagued by regular hyperinflation, mass unemployment, etc.

As a result, a common investing wisdom has emerged:

Never, ever, invest in Argentina

The wind might be changing with the election of Javier Milei, a rather … unorthodox politician who got elected on the premise of dismantling 90% of the Argentinian government, dollarizing the economy, etc.

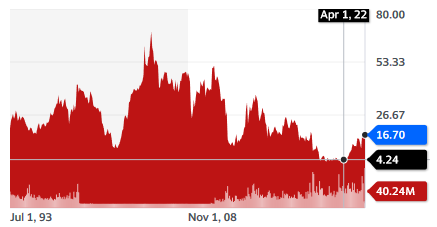

Most Argentinian stocks jumped 20% on his election, with the national oil company YPF an astonishing 40% in one day. Since its low of 2022, the stock is up 4x.

My own personal exposure to Argentina, the farmland and real estate company Cresud (CRESY) grew less from Milei’s election but has grown quite well from the 2020’s bottom.

The important part is that this gain could only be captured by buying these stocks when the stranglehold of leftism over Argentina was at its STRONGEST.

Back then, no one wanted to discuss Argentina. Even Brazil was beyond the pale for most investors.

Now that Milei is elected, I have several people asking me what I think about it.

As usual, prices drive the narrative.

Pricing In Risks

How is it that when borderline lunatic monetary and economic policy were looming over Argentina, it was the best time to invest?

For the same reason that is the basis of the good old investing adage, often attributed to the founder of the Rothschild dynasty.

Buy when there’s blood in the street (even if it’s your own)

In the years before the Milei election, Argentina was heading for another hyperinflation, mass emigration, default on its international debt, government collapse, etc.

THIS is what “blood on the street” looks like. In that case, it was quite literal.

The naysayers will always forecast a Venezuela-like scenario, with a total loss of all investments.

But the only actual question is to figure out if the risk is already priced in the current valuation.

Calculating Risks

In practice, you need to run it as a simple risk calculation:

is the risk of full communism THIS YEAR > current expected yield + chance of repricing?

In the case of Argentina, when it was really bad, the expected yearly return could be estimated at 20-100% depending on how you calculated it and the assumption.

So you would have needed a more than 30-50% chance of Argentina turning into Venezuela THIS year for the risk to not be priced in. Even the most pessimistic or right-wing-oriented commentators were not forecasting it.

Hence a potential for profit even if the situation just went from terrible to bad.

Analyzing The Situation Rationally

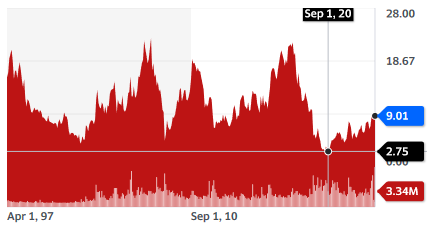

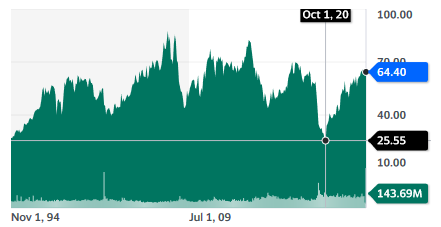

Another great example has been Petrobras, Brazil’s national oil company, in the last 2 years.

The stock price has fluctuated more according to the Brazilian political situation than to oil prices or profits. It first rose when Bolsonaro looked like he would be elected. It then crashed again when it was the socialist Lula who won the presidential election. Riots by Bolsonaro’s supporters did not help either.

And since then, Petrobras’ stock price has veeeery slowly clawed its way back up, as the apocalyptic takeover by Lula turned out to be pretty boring if anything.

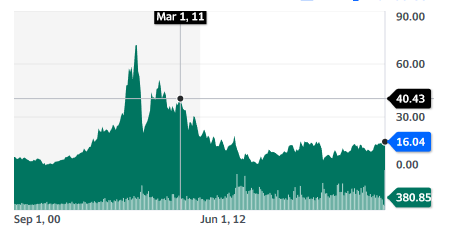

But really, was it that surprising that Lula would be somewhat irrelevant to Petrobras? During his last presidency, from 2003 to 2011, Petrobras stock rose from $5/share to $40/share, with even a spike at $70/share.

Once again, prices tend to drive the narrative.

The most repeated narrative is that Petrobras stock crashed due to “the company being looted by Lula”.

In reality, it had a lot more to do with oil & oil stocks entering a decade-long bear market, after the fears of peak oil production in 2008.

After all, from 2011 to 2020, a “safe" jurisdiction” oil stock like Shell went from $77/share to $25/share.

Trading Sentiment

The maximum gain can be targeted when the political situation is dire. South America’s politics are a pendulum, and the more left they swing, the more right they will swing back. Case in point with Argentina and its chainsaw-swinging president.

The associated theorem is that the minimum gain is when the political situation is rosy.

The more economic growth, the better the currency, the stronger the commodity markets, and the more South American masses will want free stuff.

Free education, free healthcare, free family benefits, discounted fuel, discounted food, travel, etc.

And the more it will be paid by ACTUALLY looting large companies, raising taxes, and debasing the currency.

Funnily enough, the strongest the economy, the higher the valuation multiple.

So let’s look back at that “risky” stock that was trading at a P/E of 1-3 during the socialist period.

In good capitalist times, not only this stock might be close to its peak cyclical earnings for the decade, but it will also trade a P/E of 10-20.

Earnings shrinking or multiple contractions can hammer such a stock.

If they occur both at the same time, losses of 70-90% might be on the menu.

So in my opinion, the more positive the overall sentiment, the less you should invest in South America.

Sentiment Review

In order to give some clues of what countries seem to have the most potential in the region for investors, I can rank roughly the sentiment for each major country:

Abysmal:

Venezuela. Nothing to say, the country with the most oil reserves on Earth is unable to feed its people. That’s just sad… Best target for investors as soon as it gets liberated from its dictator.

Very Poor:

Suriname: not on anyone's radar besides oil analysts. Might be the new Guyana, and its neighbors Brazil and France are unlikely to invade. Could be a replacement for Guyana (see below).

Colombia: ultra-leftist president trying to shut down the country's main export, oil + the stigma of a sticky “narco” image.

Poor:

Brazil, due to the Lula presidency. It was very poor right after the election, but improved since, as illustrated by Petrobras stock rising from $10.6/share to $16/share.

Neutral:

Argentina: thanks to Milei's presidency. Actually a mix of negative (“Argentina never changes”) and positive (“Milei is the savior of the country”). Depending on his success or failure, one opinion will be vindicated.

Peru: recent protests against copper mines and general unrest have damaged its image as a premium mining jurisdiction. But still not an overly negative image.

Guyana: used to be a positive image until Venezuela threatened to invade the defenseless nation. Due to an absurd amount of oil per inhabitant (higher than Saudia Arabia or Qatar), Guyana might have good long-term & more importantly NON-CYCLICAL growth prospects as long as it does not get invaded.

Positive:

Chile: by far the richest country in the region. A lot of risks in my opinion, with several rewritings of the Pinochet-era constitution having been rejected by both left and right. Might surprise negatively with increasingly polarized and dysfunctional politics.

Next

In the next iteration of this ongoing “investing in South America series, I will successively look at different countries and sectors, looking to give a general overview of the continent’s opportunities and cheap stocks.

This will include energy, tech, farming, and mining.