Since the oil price crash of 2014, the general consensus is that fossil fuel, ALL fossil fuel are going the way of the dodo. The only debate seems to be when the consumption peak of coal/oil/gas will occur, or even if it hasn't already happened.

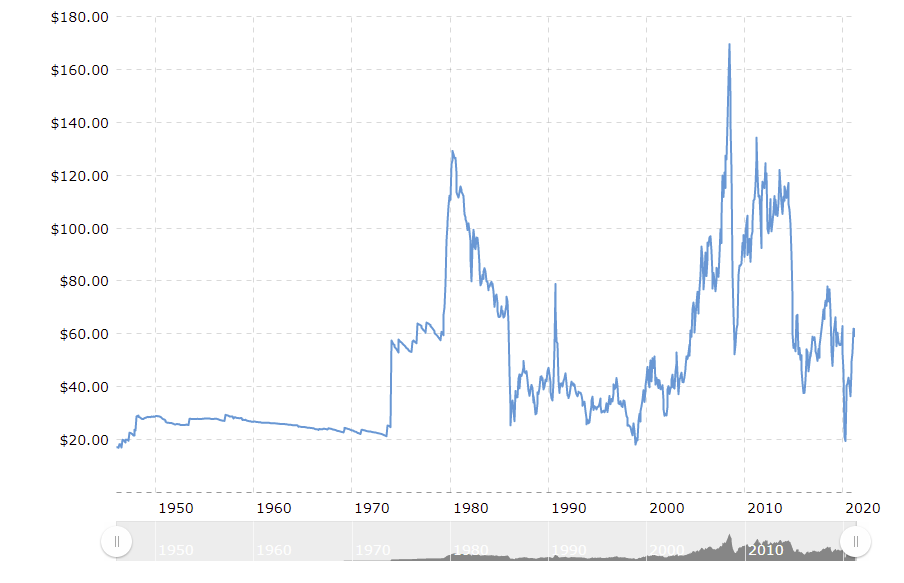

For sure, oil prices are looking set for a long term downward trend for the last 10 years (oil price in the graph below is inflation adjusted).

But not so long ago, peak oil meant a completely different thing. It meant that the world would be running out of oil despite desperately needing it. This was supposed to be the harbinger of the impending collapse of industrial societies, the final death of energy hungry capitalism and the salvation of Earth from global warming.

Not unsurprisingly, the narrative about peak oil as running-out-of-oil was at its height in 2008-2013 period, when oil price per barrel was stubbornly staying in the double digits. Other fossil fuels were not especially cheap either.

But since then, two separate events in the market have flipped that narrative.

The shale oil revolution

From 2014 onward, USA has turned from a major consumer to a major producer of oil, thanks to new methods of extracting oil from shale deposits. This spectacularly reversed a long term decline in production ongoing since the 70s.

In just a few years, oil markets would be turned upside down, as the main buyer in the world (alongside China) simply vanished and turned into a competing exporter instead.

This was the time of wild enthusiasm and euphoria for US producers. "America is back, baby!". This was the period when the US government envisioned to protect Europe from dependence on Russian energy, culminating with the often mocked freedom gas label for natural gas from the US. The overproduction of oil and gas by shale producers flooded the market and crashed price brutally. The crisis got worse when the Saudi tried (and failed) to kill shale by flooding the market even more.

Since then, markets have been convinced that any recovery in price will stimulate a surge in shale production, keeping price in a low 50-60$ range at best. With improvement in shale technology, it is even possible that the price stays permanently at 35-40$. Especially with more very large shale deposits being developed in China or Argentina and even Russia.

The final nail in the coffin of the running-out-of-oil narrative was a 2 phase price war (in 2014 and in 2020) between the 2 other main producers, Russia and Saudi Arabia, a price war which almost destroyed the OPEC.

And last but not least, oil companies were hoping for a light at the end of the tunnel in 2020. But the light turned out to be the COVID train that obliterated energy demand by grounding most flights, and paralyzing commute and travel. The glut of oil that could not be stored anywhere was so bad that for the first time in history, oil prices turned negative in 2020.

Electric transportation

I will not go into detail on how throughout the 2010s, Tesla proved that electric cars could actually be cool and fashionable. What started with a cool and expensive sports car turned the company into one of the largest (and most controversial among investors) company in the world.

Batteries kept getting cheaper, allowing electric cars to become cheaper, get more range and become competitive with ICE (Internal Combustion Engine) cars. In fact, battery costs have been divided by 6 in 10 years according to the IEA (International Energy Agency).

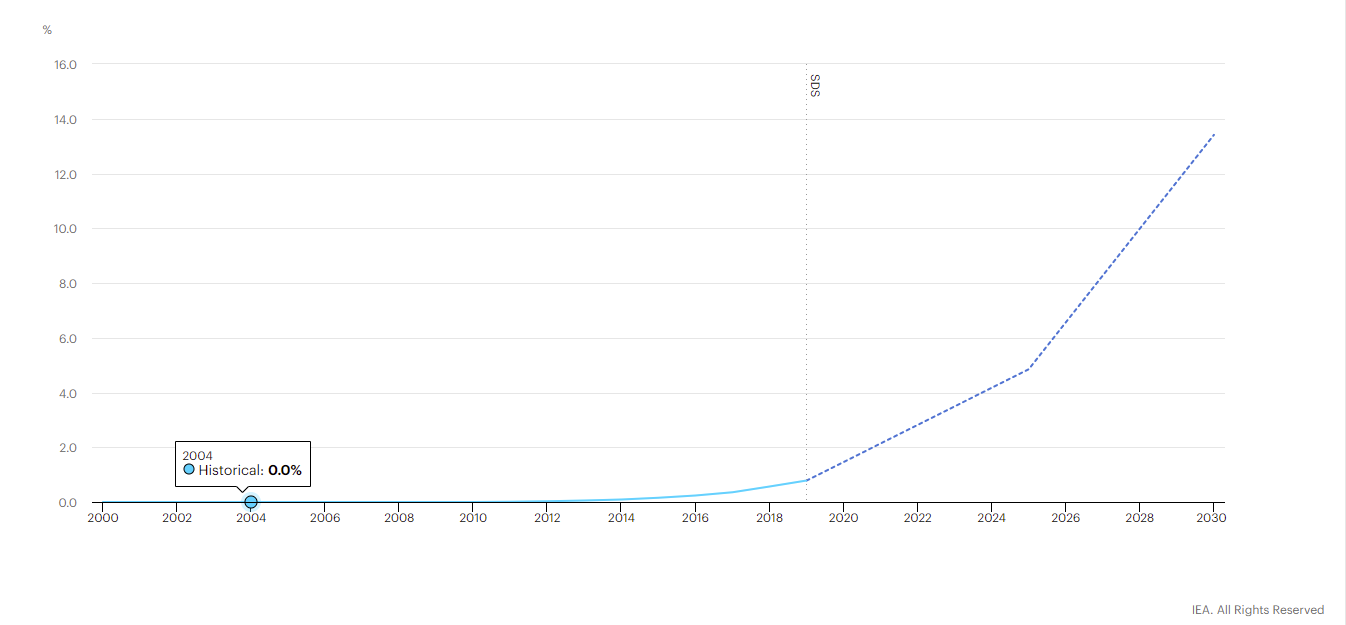

The IEA is also forecasting that 14% of the world cars will be electric by 2030, just 9 years in the future.

The consequence of Tesla's meteoritic rise and exploding valuation is that every single car maker in the world in now racing to develop its own electric car line up and many are planning to slowly give up ICE engine entirely. For Jaguar, this will happen already in 2025.

The end of oil?

So, to resume, oil & gas are being overproduced permanently, and are soon not even needed, as all transportation will soon switch to electric. On top of that, fossil fuels are just plain bad. Evil. They produce global warming-causing CO2, and any ESG conscious investor should avoid them. A common opinion in the public is that the sooner the whole industry disappears, the better.

But is any of this really true? I will actually make the case that none of these trends are as strong as the market believes.

And that for the next decade, energy might turn from the worst performing sector to the best one. As can often be expected in cyclical industries, the main focus of this blog.

The overproduction

Shale oil seems to be an unlimited and cheap supply of previously rare resources, and is believed to be the doom of traditional producers and petrostates like Russia and Saudi Arabia. So it must have been an awesome time for investors of shale oil companies, right?

Let's look for example at one of the poster children of the shale oil enthusiasm, Occidental Petroleum. The company has steadily burned through its shareholders' wallets, through unprofitable oil wells and too expensive acquisitions.

Another one, Chesapeake Energy, maybe even more spectacular. I cannot show you the chart, as it only recently came out of bankruptcy.

Bankruptcy was also the fate of many if not most of the smaller producers that kept producing until the last minute, but never turning a profit for more than a quarter in a row.

According to OilPrice, a specialized publication in the field and relaying a Deloitte report, shale oil as a sector destroyed no less than 300 billion of dollars of capital in 15 years!

Shale oil is actually a textbook case of malinvestment prompted by too low interest rate on safer investments like US bond. Starved for yield, investors invested massively (buying share and bonds) in a risky sector. It was profitless, but expected to become profitable one day, when technology reduced shale oil production cost. The promise of future profit (for shares) and attractive yields (for corporate bonds) was enough to attract yield seeking investors.

But in fact, shale oil is at best a marginal producer, as the capital invested in shale wells allow for a quick rush of production, followed by a quick decline. Production of shale declined by no less than 40-50% in the first year, instead of the 15% of a regular/traditional oil well. This means that shale oil producers need to keep drilling constantly just to keep up with production decline. And that is expensive.

This constant pressure pushed the shale oil producers to look for growth at all costs, pursuing illusory economies of scale. Or maybe not fully illusory, but the economy of scale and technological improvement have been compensated by the fact that all the prime resources got drilled first, leaving only second-class shale oil deposits that are more expensive to drill and less productive.

Combined with an industry unable to reduce output, as it was always desperate to raise more money, this both crashed global prices and guaranteed the fall of the so-called shale revolution. Shale will still be around, but the resources will now be in the hands of much more disciplined and long term focused major producers (like Exxon and Chevron), instead of hordes of short-term thinking small producers.

The missing CAPEX

As a result of the constant flux of negative news since 2014, Oil & Gas companies have steadily reduced their capital expenditure over the years. And then, alongside these already low levels, came COVID, leading to an extra $43 billion cut in capex. The reduction in expenditure was so great that all but one (Transocean) of the offshore drilling companies went bankrupt during the last years.

Energy exploration, production, transportation and refinery is a capital intensive industry. It is simply not possible to produce and transport the almost 100 million barrels per day the world needs without massive investment in drilling platforms, pipelines, tankers, refineries, storage tanks, etc...

Large projects take a lot of money, but also time from inception to production. For example, Exxon has been exploring Guyana's waters since 2015, with astounding success, and have only been ramping up production since 2019. And these discoveries should only reach full speed a few more years in the future.

This means that 7 years of anemic capex will lead to a shortage of new projects and reserves for most oil producers. Reserves have dwindled and have not been replaced, and new projects started now will only bear fruit at the end of 2020s at best.

So this should be a classical case of bust and boom in commodities, due to the long time of new projects after a period of overproduction. But markets have been assuming that by the time the effects of COVID disappear, the reduction in oil consumption from electrification will push oil consumption down permanently. So the reduced production would not lead to a cycle of rising price, as consumption will enter a phase of slow terminal decline until oil become useless.

Gas, mostly used to generate power, is expected to follow a few years later, replaced by renewable energies. So let's look at these two topics separately and see how the imminent death of fossil fuels narrative is actually overblown.

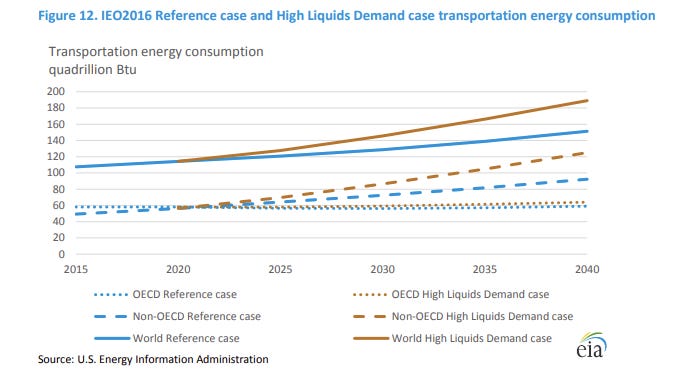

The electric menace

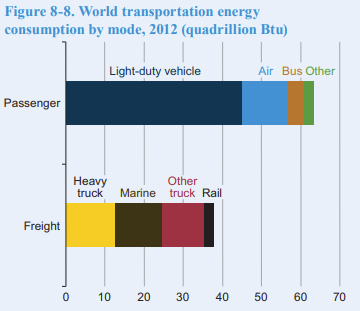

In order to understand fuel consumption for transportation, I rely on a report by the EIA. While a lot of energy is used by individual cars, they represent in fact less than half of the total energy used by the transportation sector. The rest is consumed by air, public transport, as well as truck and marine shipping. It is entirely possible that in 10 years, 10-20% of cars will be electric. Even if some electric car buyers are not so happy with that, it seems.

There is however no substitute viable in the near term for aviation or marine, and electric semi trucks are still not commercially available, even less so widely used. Constraints on lithium availability for the large batteries of semi-trucks will also be a problem.

Vehicles like planes, ships and trucks are also massive capital investments that are renewed slowly by their owners. I can imagine 30 years in the future a transportation industry running on electric batteries and/or hydrogen. But any shorter time frame is simply unrealistic. Until 2040, oil consumption is simply here to stay.

Can it be reduced in volume by electric cars and buses? I imagine so. But for the rest?

Trucks might be the first to evolve to electric / hydrogen solutions, but the renewal of the existing fleet will still take 20+ years. Until the whole fleet is actually switched, fuel consumption will only be marginally impacted.

Ships might switch to liquefied petroleum gas (LPG) first before totally giving up fossil fuels.

Planes need a fuel density that batteries are simply unlikely to provide for quite few more years. At the moment, there is no alternative even being developed for large carriers, and even less chances of most flights to run on electric in one or several generations.

Overall, the extraordinary technical achievements of Tesla have clouded the vision of the market about electric transportation. While the cars you see downtown are the most visible thing, the truth is that most fuel is used to move goods on the ground, sea or by plane. And that consumption is here to stay, and probably even grow. In fact, the total energy used for transportation is expected to steadily grow. So even if a growing percentage of that energy becomes carbon neutral, it might just offset the growth in consumption, but not really reduce the volume of fossil fuels used.

Ultimately, the aim to go carbon neutral by 2040 of many countries, including the EU block, will need something more than electric cars. Most likely, these goals are totally unreachable without some form or another of carbon capture technologies.

The power of renewables

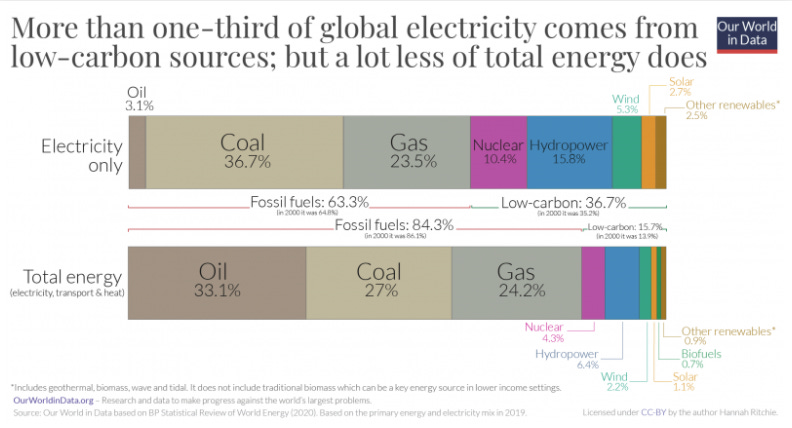

So, electric power is assumed (a misguide assumption) to soon replace oil consumption. But even if this was fully true, where is all that electricity going to come from? I found this very illustrative image from Our World in Data.

Just to replace oil in transportation, as well as coal and gas for heating, it would require to almost double electricity production. That's a lot of power plants to build in a record time.

Low carbon = renewable?

At first glance, 36.7% of low carbon electricity worldwide seems like good news. 1/3 done, 2/3 to go... right? But actually, most of this low carbon production comes from either nuclear or hydropower. Respectively 10%+16%=26% of the 37% low carbon power generation.

Hydropower is probably the cleanest electricity production method. It is also VERY cheap per kilowatt, and the operators can to some extent decide to activate it on demand. But it relies heavily on geography. Even ignoring the damage done to aquatic ecosystems, dams can only be built in specific locations, and most of the best ones are already used. And some countries are completely unable to use that power source as they are flat, like the Netherlands or the Baltic countries where I myself live.

Nuclear could be the solution to replace coal and gas. But let's admit that after Chernobyl and Fukushima, nuclear energy has somewhat of a PR problem. With the exception of France, Russia and increasingly China, very few countries are even willing to look at nuclear power as a major electricity source.

Public opinion might change about it slowly, as people realize that nuclear IS very low carbon. But considering that new nuclear power plants take 10 years or more to be built, we are unlikely to see them replace fossil fuels over the next 10-20 years. In the long run, this is the type of energy I think makes the most sense, especially thorium and small modular nuclear, but none of these will become generalized in less than a decade.

Solar and wind

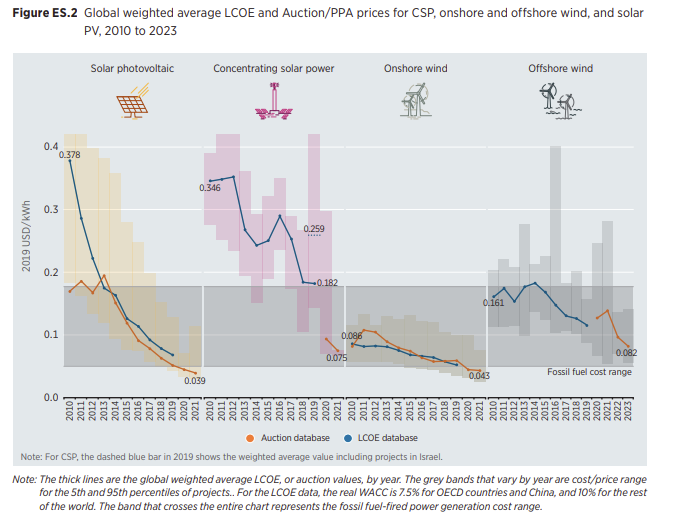

Of course, the obvious and most popular solution is to increase solar and wind power. They have indeed gotten cheaper and cheaper each years, and are now competitive with fossil fuels according to the IRENA (International Renewable Energy Agency). Indeed, photovoltaic for example, got 82% cheaper between 2010 and 2019. In the graph below, the grey zone represents the cost range of fossil fuels.

Can that cost reduction continue?

When it comes to solar, the problem is that most of the cost decline has been a reduction in the price of the solar panels themselves. Now that the panels are becoming just one of the cost of a utility-scale solar plant, such gains are likely to slow down. The other costs like land, manpower, capital, other materials, etc... are much more likely to stay the same or increase over time.

For wind power, the likely problem is mostly that the most promising sites are already used, and second-class sites are likely to be less productive / more costly. There is also some real question about the total energy needed to build a wind mill (due to the large amount of concrete and steel needed) and the impossibility to recycle the blades, that are simply buried in giant landfills. I could not find a copyright free image of it, but follow the link and tell me if this looks sustainable...

But overall, considering the push for low carbon energy, renewable seems to be able to compete with fossil fuels and getting cheaper, so no problem, right? We just need to build more of it and shut down the polluting power plants and solve the smaller issue of recycling.

The intermittence issue.

There is still one tiny detail that needs to be discussed about renewable energies, before they make fossil fuels obsolete.

They don't work.

At least not all the time.

Solar obviously does not work at night (duh!) and a windmills need... wind. I hesitate to adopt such ironical tone on this paragraph, knowing how people get worked up on this subject. Do I really hate the planet, the rainforest and koala bears?

Well no. But for some reason, people brush aside the problem of renewable's intermittency. The conversation usually goes this way:

"It just needs more storage."

"What form of storage? How much does it cost?"

"It is not going to be a problem, batteries are getting cheaper. Solar is cheaper than gas already, don't you know?"

"But how much is the storage costing. If storage is needed for solar, shouldn't the storage cost be included?"

"But fossils fuels have subsidies too..."

I truly would prefer a world powered by a mix of hydro (and nuclear) with some solar and wind power on top. But in practice, renewables are highly intermittent. Not only solar does not produce anything in the evening, at the moment of peak consumption, but it also produces very little in the cold season. When you need a LOT more power for heating, especially if you stop using gas.

When it comes to wind power, it can be powerful when it the wind is blowing, but can also dry out entirely for weeks at time. Batteries might be enough to cover the gap during the night, but the amount needed to cover weeks of a whole country is simply staggering. It would probably require tripling or quadrupling the amount of capital needed for the electric grid (more on that below). Hence, wind power can only stay a small part of the whole energy mix, probably not more than 10% maximum. If do not believe me, listen instead to the Royal Academy of Engineers in UK, who warn that within 5 years, Britain might face electricity shortages in winter, due to wind short spells. The California grid operator is issuing the same type of warnings following blackouts.

The real cost of storage

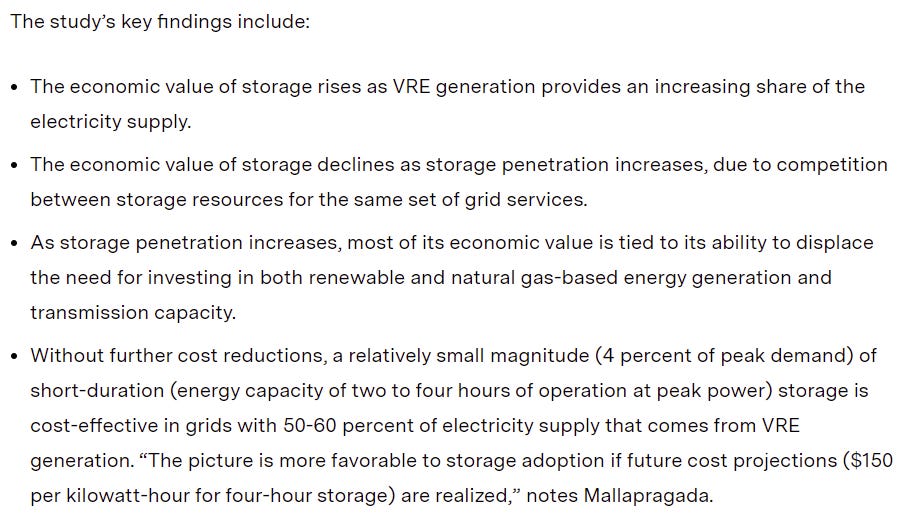

So what is the real cost of storage per kW to solve the intermittency problem? Surprisingly, it is hard to find some hard data about it. Even with very large storage facilities being already built, like in California.

From an MIT study, it appears that the more storage is being built, the more capacity needs to be added. And the more storage is added, the less productive / the more costly it gets, despite being required to maintain the stability of the electric grid.

So the more storage is needed, the more expensive it gets. This alone might negate a lot of cost reductions from improvement battery technology. In the report's own assessment (VRE = Variable Renewable Energies):

So the threshold of VRE (wind and solar) after which storage cost grows exponentially is around 50-60% of the electricity production. A fully carbon-free electric grid would cost way more in terms of storage than a partially renewable grid.

After a (very) long time researching the subject, I got a bit desperate to find you actual numbers that would indicate by how much the cost of renewables would be increased if taking honestly into account the unavoidable need for storage.

I could find a lot of studies showing how much X hours of storage would cost per year. What I could not find is how much it would impact the production cost of renewables. Would batteries cost increase solar and wind production cost by 10%, 100% or 500%?

Until I finally found it, but frankly, the deafening silence on the topic make sense, because the numbers are just plain bad. In a 100% VRE grid, the replacement of 1GW of production with nuclear or fossil fuels would need not only cost the price of the new solar panels or windmills, but also require an extra 3-4GW of storage to be installed. And on top of that, new transmission line would also be needed.

The same Wood-Mackenzie study tell us that for the USA only, not counting the rest of the world.

The costs of new wind and solar units needed for a 100-percent renewables standard would be about $1.5 trillion. Adding the required battery storage would raise the cost to about $4 trillion and adding new transmission lines would increase the cost to $4.5 trillion.

So when we are told that going fully green will only cost $1.5 trillion, and costs are competitive with existing fossil fuels technology, it is simply not ture. In fact, it is pushing under the rug $9.5 trillions of extra costs for the electric grid (denser grid + storage). Or just 86% of the total cost.

Such fully "green" grid might still be a lot more brittle than expected in case of conjunction of bad conditions, like a perfectly normal cold spell + no wind + cloudy weather. Not something out of the ordinary in winter in the northern hemisphere. The recent Texas disaster, which apparently might be one of the most expensive events ever for the insurance industry, shows us the dramatic effects an electric grid collapse in winter could have.

On the subject of storage, I will also note that other technologies than batteries, from pumped-hydro to gravity well to flywheels are being studied. So far, most of electric utility companies seem to think only batteries have a sufficient capacity + low losses on a series of charge-discharge cycles to be used routinely to stabilize the electric grid in the future (pumped hydro is also used now, but cannot be widely expended for various technical limits). So I will leave these alternatives aside to not make this article even longer.

So when storage is not conveniently forgotten, the dream of a fully 100% green electric grid is unrealistic, especially by 2030 like the Green New Deal proponents want us to believe. But considering the costs, even by 2040 I am skeptical this is doable. Especially if nuclear does not do a come back to provide the baseload power.

So no end for fossil fuel?

After a rather long study resumed above, I came to the conclusion that the world is not going to stop consuming fossil fuels any time soon.

Oil is too embedded in transportation, and often impossible to replace in less than a few decades (like for ships and planes).

Gas is likely not really in danger from renewable, and might even grow as coal power plants are slowly being converted to gas-power plants.

Nuclear should be a serious competitor, but public opinion and regulatory framework will block it from expending significantly.

Intermittent renewables will keep growing, but the larger their part in the energy mix grows, the more storage costs and grid brittleness will slow its growth.

Some other renewable energies, primary geothermal and hydrogen, might start to dent fossil fuels dominance in the 2030s, but will likely not be really important before 2040.

After 2040, I can easily accept the possibilities of a gradual replacement by cleaner energies. Renewables will have gotten really cheaper and more efficient. Batteries are likely to be way more efficient and recyclable. And nuclear (especially thorium), geothermal, or even space-based solar (using reusable rockets) might be able to finally offer us a solid alternative to the carbon economy.

Oil & Gas companies are now priced for imminent failure and the complete death of the sector in 10 years. I think this is a mistake of taking a negative trend in the far distant term future for an immediate reality. The same way that Tesla is now worth more than the entire automotive industry because "it is the future"...

But in the (maybe properly attributed, who knows) words of Mark Twain, I think Oil & Gas can equally declare that "The reports of my death are greatly exaggerated."

In the next reports, I will look into energy companies that are positioned optimally to catch the moment when market realizes energy production is indeed changing, but not as quickly as expected.