A lot of digital ink has been spilled writing about the Magnificient Seven (Google, Amazon, Apple, Meta, Microsoft, Nvidia, and Tesla).

Overall, it can be said that the US stock market has rarely been as overvalued as it is now since 1929 (if ever). The same can be said for such a top-heavy market, with the largest stock driving most of the growth of the S&P500.

And that the US stock market has only been that concentrated in tech since the Dot Com Bubble.

And that many of these stocks are INDIVIDUALLY getting close to be worth more than most countries’ ENTIRE stock markets. Do you want to own Apple or all listed German stocks? The Magnificient Seven or ALL of the listed Chinese stocks?

Let's just look at a BarChart infographic for a more visual example:

Overall, hardly good parallels to go by.

So what can be done for investors looking at Nvidia making new all-time highs almost every day? Join in the fun? Or stay on the sidelines and struggle to keep up?

First I will discuss the Mag 7’s likely prospects and issues. And then look deeper if their profits are real.

Remember: No Shorting

The very first thing to remember is that you should not try to short the Magnificent Seven. That’s a lesson you would think people learned from years of Tesla going crazy high.

But still, I see plenty of otherwise good investors burning money in stubborn bets against an irrational market.

Record Profit?

The argument to support that such stratospheric valuations are justified is that these companies are insanely profitable, are still growing, and extremely innovative.

In my opinion, all 3 of these are dubious at best.

Growth Potential?

The first part is to discuss how much more growth can be achieved. When you are a 1 to 3 trillion dollar company, growth is becoming a little harder. The quantity of extra iPhones, cloud subscriptions, or electric cars you need to sell to keep doubling in size is rather daunting.

A good case can be made for each of the Magnificient Seven that the era of explosive growth is over:

Tesla: compressing margins and the arrival of cheaper Chinese EVs described by the Western auto industry as an “extinction event”.

Apple: not much innovation since the death of Steve Jobs, and the VR market is much smaller than smartphones, and that’s likely permanent.

Nvidia: margins are at all-time highs, competition is catching up, and all the tech giants are building data centers en masse. If the build-up volume for AI keeps going for a decade at this pace (need to justify the current valuation), there will simply not even be enough power generation to use them. AI might be made of virtual bits, but it needs to burn a lot of atoms to run.

Facebook: Social media are pretty much saturated at this point, everybody who wants to be on is already there. Not sure if TikTok is an actual threat, but it does not help for sure.

Amazon: Amazon is failing to be number one in most international growing markets: China, SE-Asia, South America. And its one Western turf is now under pressure from Shein, Temu, and Alibaba. Cloud is now the real money maker compared to e-commerce, but even that is a highly contested space.

Microsoft: Funnily enough, the least discussed of the 7 is probably the best one. Both its AI and VR efforts are focused on the better use cases of B2B and enterprise segments, and the videogame aggregation keeps going with the acquisition of Blizzard.

Google: after 2 decades of tremendous R&D spending, 80-90% of revenues are still … search, now under pressure from LLMs. Considering the launch of their AI Gemini turned out to be a reveal of how racist, pro-pedophilia, and generally woke it is (a reflection of a growing problem at the company), I am skeptical of it turning into a revenue driver any time soon.

Each might manage to keep growing, but they are all facing the dual issue of being already very big and seeing competition catching up. And for some like Google, clear signs of internal sclerosis and bureaucrats/ideologues taking over the company.

Innovation?

While each of these companies can still be (?) called innovative, it is questionable that they are still efficient at it. That’s because they are collectively burning through hundreds of billions of dollars to give the following results:

Increasingly less functional and more ideological search (including with AI). The same can be said for chat apps, voice apps, etc.

Not the cheapest e-commerce, nor the best-performing smartphones, nor the most innovative EV, or the best self-driving cars, etc.

With each of these categories increasingly dominated by Chinese firms (Pinduoduo, Alibaba, Huawei, CATL, BYD, etc.) that need to be kept at bay with tariffs, as open competition would not favor the Mag 7 stocks.

Entire segments of very important innovation have no large Western players, especially everything hardware or science-related: drones, batteries, solar panels, nuclear tech (thorium, SMRs, etc.)

Increasingly iterative “innovation” instead of revolutionary. Smartphones are 2 decades old, EVs are now a highly competitive (and money-losing) industry, e-commerce is done by everyone, and AIs are still to prove they can make money out of B2B cases and fundamental research.

Progressively, innovation by the West and the Mag 7 in particular has started to mean software, apps, AIs, etc.

The only real hardware & highly innovative companies left are linked to Elon Musk alone (Tesla’s EVs, Space X’s rockets).

This was further confirmed by the recent announcement that Apple gave up 16 years of efforts to make an EV, redirecting 2,000 people that seemingly produced very little results.

Profitability?

The innovative capacity or market potential is rather subjective. I am sure some people will feel that VR and AI are big enough to justify the current valuations.

What is more concerning is the argument that the Mag 7 companies are highly profitable.

The truth seems to be that many are engaging in deceptive accounting practices, especially vendor financing and circular investing/self-dealing.

Vendor financing

Vendor financing is the practice of giving upfront your customers money so they can buy from you. This is an easy way to grow revenues, especially if you have access to cheap capital in the form of debt or overvalued equity.

Of course, said customers will need to pay it back, so you better hope that they are profitable or can raise more money.

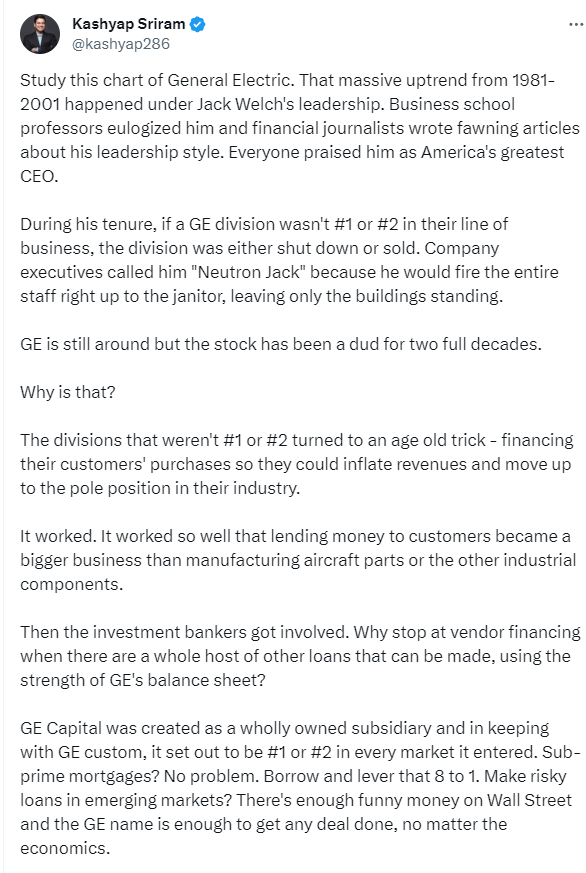

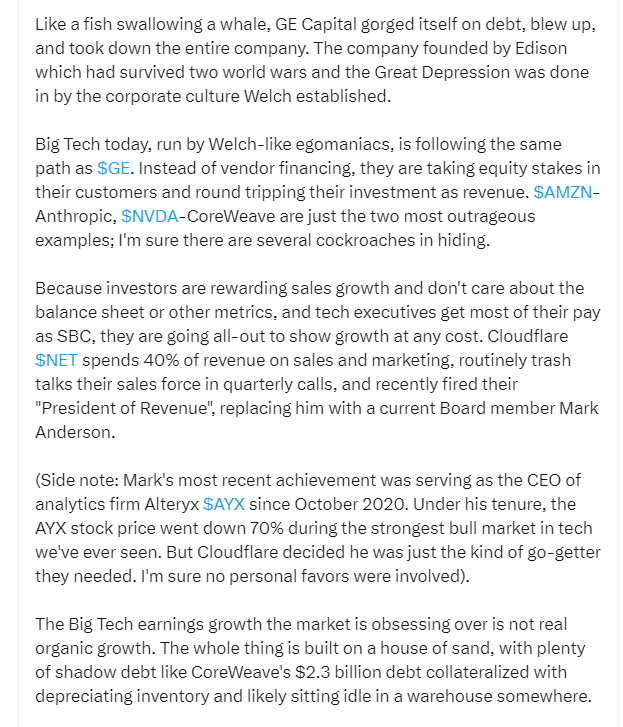

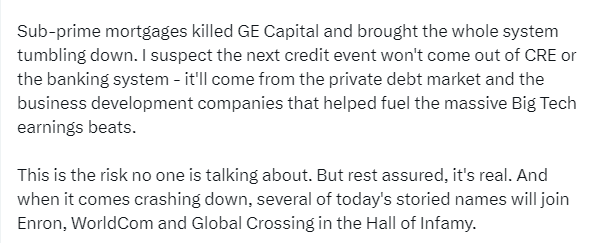

This was a specialty of GE when it steadily eroded its position as an industry leader. The Twitter post below explains it well, as well as why it happened:

The pressure to be #1 or #2 at GE is today in Big Tech replaced by the need to show steady growth at all costs. But the logic is the same.

Short of specific cases, vendor financing is the equivalent of taking a shot of cocaine before running a race. Do it once and it might give you a boost which, while unhealthy, will probably be okay. Do it continuously, and you might get problems. The problem of doing it only once is that it is addictive of course…

The most guilty of this seems Nvidia, while the others are not innocent either.

Self-Dealing

Big Tech companies invest a lot in smaller tech companies. In itself, this is a sign of the industry getting mature, similar to how Big Pharma essentially subcontracts innovation and is now specialized in marketing, mass production, and regulatory capture / lobbyism / corruption.

But in the case of Big Tech, the money has a wonderful way to come back home. You might get X billion from it, but you need then to buy their hardware, their cloud solution, their software, innovate with their AI, etc.

In itself, this is not necessarily a bad thing. But the issue is that it muddies the water in understanding the real demand. How much of the current demand is real, and how much is just a subsidy where money is essentially counted twice?

(still from Kashyap Sriram)

Dealing With The Tech Supernova

The problem the Magnificent Seven poses to investors is two-fold.

I. First, there is the issue of lagging behind if you do not own them. This is only mentally painful for individual investors but can be career-threatening for professional money managers.

II. Second, they are SO big that if that bubble ever pops, it might take down a lot of unrelated sectors with it. So just not owning them is not enough to be out of the blast zone.

Benchmark Issues

The first problem can be dealt with differently depending on your position.

Individual investors should simply not compare themselves to a benchmark. This is more a matter of discipline than anything else. Target a realistic rate of return depending on your profile and acceptable risk and tolerance for volatility (anywhere between 5-15% is likely still reasonable).

For money managers, this is trickier. One option is to hedge by buying out-of-the-money options on the latest high runner among the Mag Seven. It used to be Tesla, then Facebook, now it seems to be Nvidia. I would expect sentiment to turn to Microsoft or Apple next. This can be expensive if it goes wrong. But then you can probably still save your job, as you can blame a general bad period in the markets.

Another option is to communicate well enough with your client about why you are not invested in the Mag 7. Riskier, but more honest and might bear fruits later on.

Taking Cover

I assume most of my readers are not the type to be all in on tech stocks. If you are, please tell me more in the comments, I am curious about the reasoning.

If you’re not, you might be more than a little concerned by every macro indicator flashing BUBBLE in the midst of a seemingly impending collapse of the Ukraine frontline, escalation in Lebanon and Yemen, and overall not the greatest time for the West’s power, economical and political.

Here are some of the measures to take that should soften the blow:

Invest in out-of-favor sectors: cannabis, tobacco, oil & gas, Colombia, etc…

Invest in cheap stock WITH HIGH DIVIDEND YIELD: cheap can become even cheaper. But if you collect a double-digit dividend yield, do you even care about capital losses?

Great Depression 2.0? Probably Not.

Lastly, I wanted to share a thought regarding where things might go.

Inflation is probably not beaten yet, and going on a war footing while still underinvesting in commodities production is a recipe for more inflation; so are increasingly inefficient energy systems.

This should, in theory, combined with a 1929-style bubble, be able to usher a crash like the one that induced the Great Depression.

In practice, this is very unlikely.

Every person with hands on the lever of macroeconomic power is a firm believer that the Great Depression occurred due to too little demand and stimulus.

They have been very busy being sure that no matter how tremendous the losses on bonds or commercial real estate, the banking sector gets enough money flowing.

So while it is always possible to see the Mag 7 bubble (and yes, it is a bubble) deflate out of control, I am skeptical it will happen.

More likely than not, we will see a few trillion printed to keep the music playing.

The question of course is what are the consequences.

Since 2008, it seemed that no matter the scale of money printing, it never mattered. Until a war in Ukraine combined with the Covid money printing made inflation explode.

So we are in a new era when money printing triggers inflation.

It should trigger higher rates, but at some point, higher rates trigger a banking crisis, and we can’t have that…

When confronted with, on one side, keeping the banking system running and the Western governments solvent, and high inflation on the other side, which do you think the Fed and the ECB will choose?

Does It Even Matter?

So ultimately, it is probably pointless to fret too much about the Mag 7 bubble.

Yes, it might pop, and it is generally unwise to join a bubble in its purely maniacal phase.

Like when Meta goes up 10% in a day because it FINALLY gives a paltry dividend.

Or the Nvidia chart looks like this, making the crypto mania period look reasonable (hence the out-of-the-money options hedge if you really feel like you cannot ignore it, either for psychological or career reasons).

But it might also never really deflate. The pressure valve will not be stocks deflating, which would make the rich poorer (we can’t have that) but currencies going the way of the dodo.

An alternative would be to cut spending, pay back the debt, and start acting reasonably.

Yeah, right…

At this game, I would expect the Euro to be an extinct species WAY before the dollar. And the dollars to flow until their eventual demise to defense stocks.

Why? Well, it is not as if the combined threat of Islamism (and inflaming by the Gaza war), deindustrialization, and war were working at the same time.

Which makes me think I need to call again a real estate agent about some 5 hectares of woodland nearby, selling at a cheap price…

What do you nean by: "And the dollars to flow until their eventual demise to defense stocks.

Why? Well, it is not as if the combined threat of Islamism (and inflaming by the Gaza war), deindustrialization, and war were working at the same time" ?