Turning Winds (part 2)

The Potentially Interesting Stocks In the Solar Industry

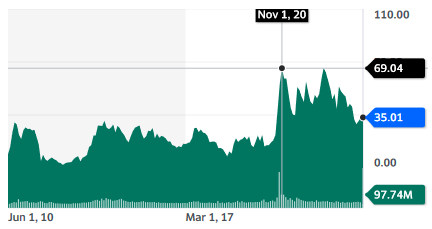

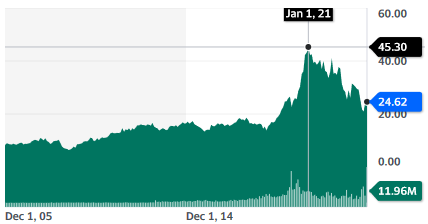

Jinko Solar (JKS)

P/E 3.43

Dividend: 4.28%

One of the largest solar panel manufacturer in the world. From this company, hard to see the decline in orders and clogged warehouses in Europe.

Probably because it still sells very well in China and Asia and other regions. Its N-Type panel seems to outperform as well, with record conversion yield of solar power.

Can this growth persist? Maybe not. But for sure, this does not seem on a surface level to justify a P/E below 4. And the dividend yield is decent considering this is a high growth company.

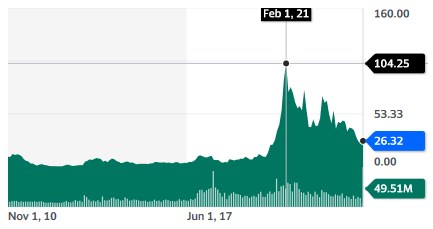

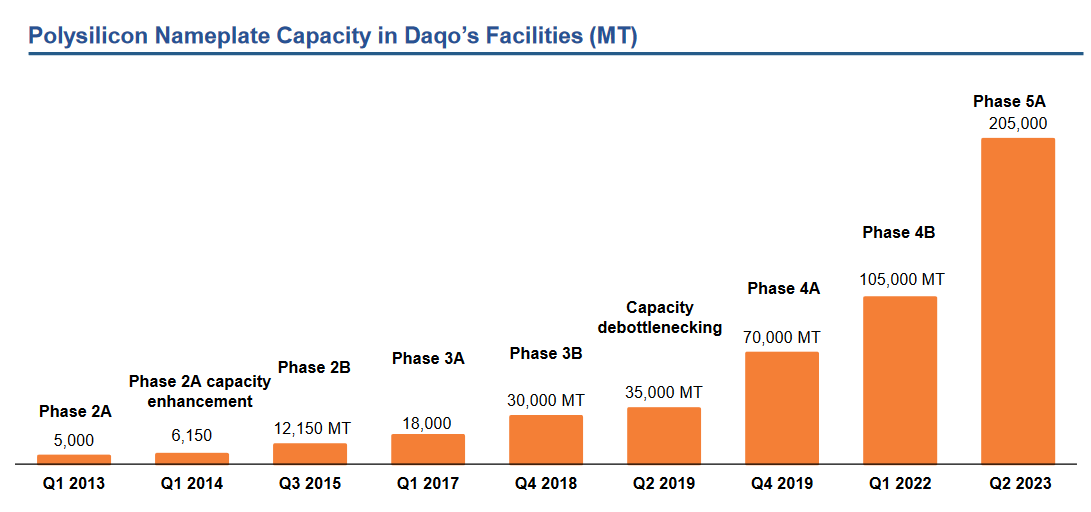

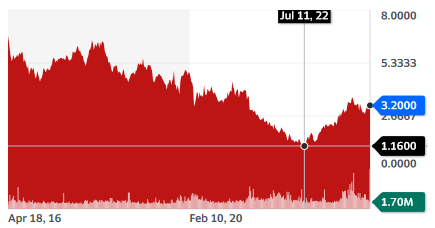

Daqo Energy (DQ)

P/E 2.98

Dividend: -

The leading manufacturer of polysilicon, the base component of solar panels. It has also among the lowest production costs in the industry, thanks to its scale. This should somewhat protect it in case of a decline in demand and polysilicon prices.

Here too, volume sold has grown, but margin has collapsed, with polysilicon costs stable around $6,5-7/kg, but the selling price having fallen from $12.33/kg a year before to $7.68/kg. This is still a 14% gross margin, but a far cry from 2022’s 80.2%.

On one hand it is flooding the market with massive production capacity increase. On the other hand, having one of the lowest production costs, it is probably pushing its competition out of business doing so.

It is still falling like a rock, and might be a good pick when sentiment bottoms. For now the combo of China + solar seems a highly toxic idea to the market. I suspect this will keep getting worse for a few more months at least.

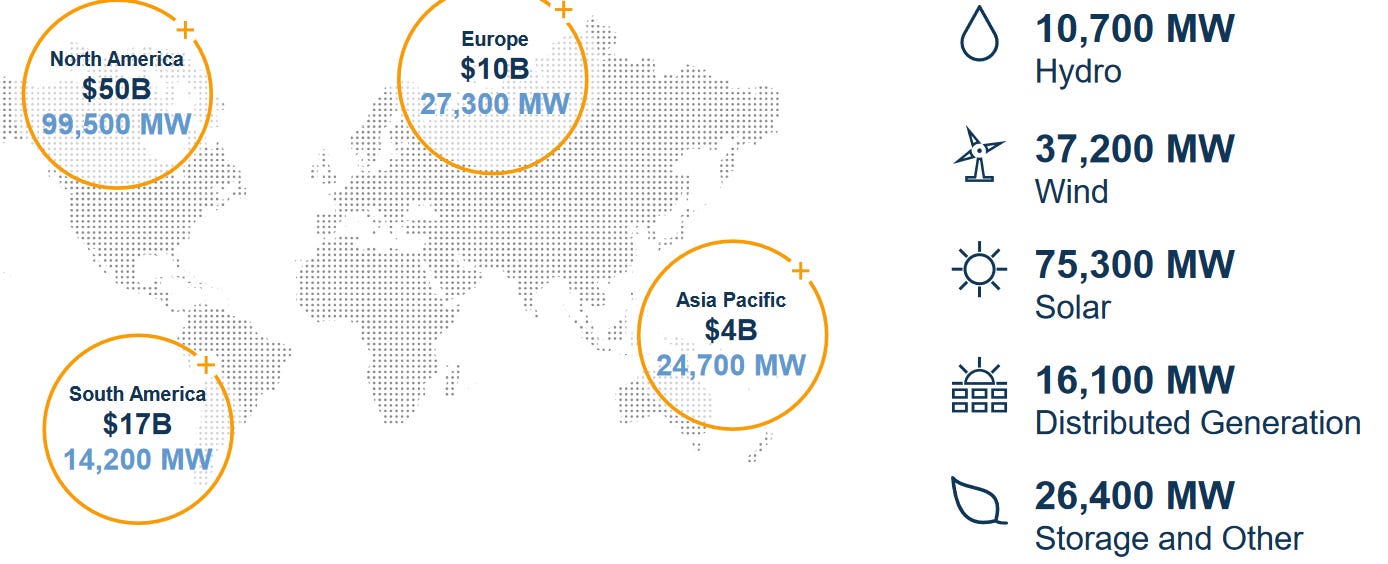

Brookfield Renewable Partners L.P. (BEP)

P/E -

Dividend: 5.48%

A giant in renewable energy production, the company is part of the even larger Brookfield Holding, which handles hundreds of billion of funds.

The group as a whole is down in the last 12 month due to rising rates. The company previously has grown distribution by 6% CAGR.

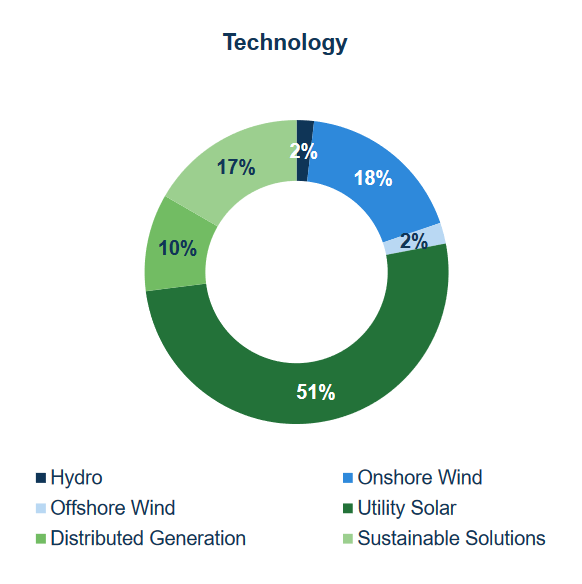

A little too much wind for my taste, but at least these are older models meaning that any early failure will be paid for by the turbine manufacturers.

The pipeline is focused on solar, even if onshore wind tends to be a bit high.

BEP also now owns half of Westinghouse, the leading nuclear power plant builder in the US, together with uranium miner Cameco (CCJ).

Very high quality company, good management, it might suffer from re-rating and slowing down of growth due to less capital available. Still, with current stock prices, didivend yield is rather high for a utility company.

Enel Chile S.A. (ENIC)

P/E: 2.78

Dividend: 10.51%

For now, my favorite utility, partly because of its yield.

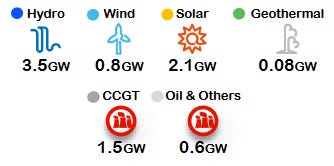

And on top of doing some solar, it is also a massive hydropower utility, and one of the largest electricity providers in Chile, as as well as an important grid operator.

Hydropower (and legacy fossil fuel power plants) are also a lot more flexible, so they can be kept for the evenings when solar stops working. Extra investments are being used to made hydro and thermal power more flexible than it currently is.

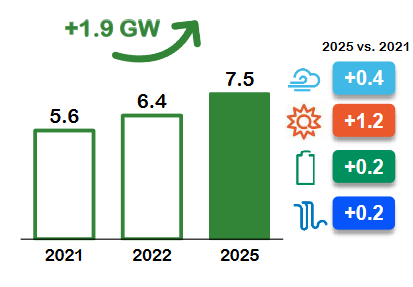

Most of future capacity growth will be from solar:

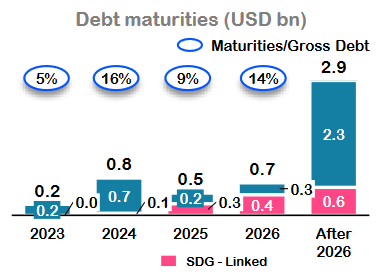

Between hydro, a perfect inflation protection (already paid ultra durable assets with low maintenance and no “fuel” costs, selling electricity that usually keeps up with inflation), and debt schedule mostly in the distant future, I like Enel Chile quite a lot.

Frankly, the only reason it is not in my portfolio is that I felt the upside of oil & gas was higher, as well as the dividends I could collect.

But if you want a slightly more defensive and less risky income focused portfolio than going all in on Petrobras and Ecopetrol, Enel Chile is probably a good option.

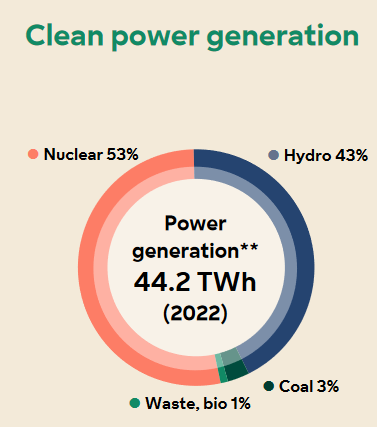

Bonus Stock: Fortum (FORTUM.HE)

P/E: 24.63

Dividend: 7.36%

The last one that caught my attention when researching this article. It is NOT a solar stock, but I felt I should share it with you anyway.

This Finish/Swedish utility simply has one of the best power generation profile I have seen, half-half hydro / nuclear.

I understand some assets in Russia are getting seized, so there is maybe more digging needed.

It might also be a great company to own if you want exposure to a cold European winter, or an energy shock due to unreliable supply from the Suez canal and the Middle East at large, in the context of the war in Israel.

Both Finland and Sweden are nuclear friendly countries, with Sweden planning a massive expansion of its nuclear fleet, so it is also maybe a good play around nuclear renaissance in Europe.